The private equity LP GP structure outlines the investment process of a private equity fund, which includes limited partners (LPs) investing in the fund and general partners (GPs) determining investment selection and overseeing fund operations. It is a fundamental aspect of every private equity professional course and is crucial for any professional in the private equity, institutional investment, or corporate finance sector to understand.

What Is the Private Equity LP-GP Structure?

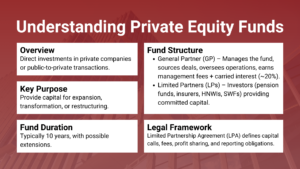

The legal and operational arrangement in which a private equity fund is organized, capitalized, and managed. It separates capital providers (LPs) from fund managers (GPs) in a limited partnership agreement that sets out the roles, economics and governance of the fund over its lifecycle.

In reality, an LP-GP structure separates the partners into two categories – LPs have limited liability and a passive ownership interest, while the GP is the active partner and investor who makes all the investment decisions. This separation is what enables institutional investors to put money into private equity without taking on the management of the fund.

Why Is the LP GP Structure the Foundation of Private Equity Funds?

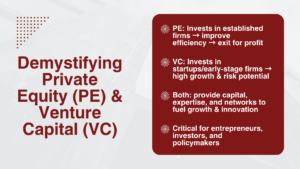

This LP–GP model addresses the fundamental private equity problem of how to pool together large amounts of institutional capital and focus investment power on one manager, who is an expert in the field. It provides a scalable investment product that can be used to invest in the same type of illiquid and high-return assets that can’t be accessed on the public markets.

If this structure did not exist, pension funds and endowments, along with other institutional investors, would have to source and value deals themselves, which they lack the deal sourcing network, valuation expertise and operational skills to do. The LP–GP model allows the capital provider to the LP to outsource this complexity to the GP and provide contractual protections to the LP through the LPA.

Table 1: LP vs GP Roles Comparison

| Attribute | LP (Limited Partner) | GP (General Partner) |

| Function | Provide capital to the fund | Source deals and manage investments |

| Legal Liability | Limited to capital committed | Unlimited liability as a fund manager |

| Investment Control | None — passive investor | Full authority over investment decisions |

| Return Profile | Preferred returns + profit share | Management fees + carried interest |

| Capital Contribution | Typically, 90–99% of fund capital | Typically 1–2% (GP commitment) |

| Governance Role | Advisory committee participation | Full fund governance and reporting |

Who Are Limited Partners (LPs) in Private Equity?

Limited partners are the investors who fund a private equity firm and are at risk of only losing the amount they invested. The most common types of LP include pension funds, sovereign wealth funds, endowments, insurance companies, family offices, and fund-of-funds. LPs invest the bulk of a fund’s capital (95-99%) to receive a passive stake in the fund and a preferred return on investment.

The LPA determines the nature of LP rights. LPs are not involved in everyday investment decisions, but larger institutional LPs may be granted seats on a Limited Partner Advisory Committee (LPAC), which oversees conflict-of-interest issues, fee changes and key-man provisions. LP rights and obligations are a skill acquired in professional private equity training that is useful.

Who Are General Partners (GPs) in Private Equity?

The role of the general partners is usually that of the private equity firm or an appointed management firm, which is in charge of raising capital, finding deals, making investments, managing the portfolio companies, and distributing returns to LPs. GPs are free to choose how much to invest – and have unlimited legal liability as the fund’s managing partner.

GPs will typically invest 1-2% of capital in the fund as a GP commitment, thereby aligning their economic returns with LP returns. This skin-in-the-game stipulation conveys belief in the fund concept and is a typical part of the LPA. GPs earn money from management fees while they are invested and carry interest on successful exits.

How Do LPs Contribute Capital to Private Equity Funds?

LPs do not contribute all of their capital commitment at the closing of the fund. Rather, the GP calls down capital in stages as the investment proceeds. After the fund is closed, LPs commit money at the close of the fund (a legally binding agreement) and are called to provide money when the GP is finding and closing investments.

A common PE fund that has USD 500 million in commitments can raise in 10-15 phases across 3-5 years. This staged reduction enables LPs to retain liquidity in other assets while waiting for the capital to be in use and gives flexibility to the GP to access the capital when a good offering comes along. An LP’s failure to answer a Capital Call within the designated period of notice (usually 10 business days) is an LPA default.

Table 2: Capital Flow in a Private Equity Fund

| Stage | Activity and Capital Flow |

| Capital Commitment | LPs sign the LPA and pledge capital — funds are not transferred yet |

| Capital Call | GP issues drawdown notices; LPs transfer committed capital in tranches |

| Deployment | GP deploys capital into portfolio companies over the investment period (typically 3–5 years) |

| Value Creation | GP works with portfolio companies to grow EBITDA, reduce debt, and improve margins |

| Exit | GP exits investments via sale, IPO, or recapitalisation |

| Distribution | Proceeds are distributed to LPs first (preferred return), then the GP receives carried interest |

How Do GPs Manage and Deploy Capital in Investments?

Upon call, GP invests the capital into portfolio companies within the limits of investment restrictions from the LPA and the investment strategy of the fund. GPs have a formal investment committee, which usually reviews and approves each investment, and extensive investment memoranda, valuation models, and due diligence documentation.

The disciplined capital deployment process includes deal sourcing, initial screening, due diligence, investment committee approval, deal structuring, and closing. In buyout funds, GPs leverage up for acquisitions, enhancing expected returns on the portfolio companies. The private equity process can be executed from financial modelling to deal execution by the fund managers with formal training.

How Does the Limited Partnership Agreement (LPA) Define the Structure?

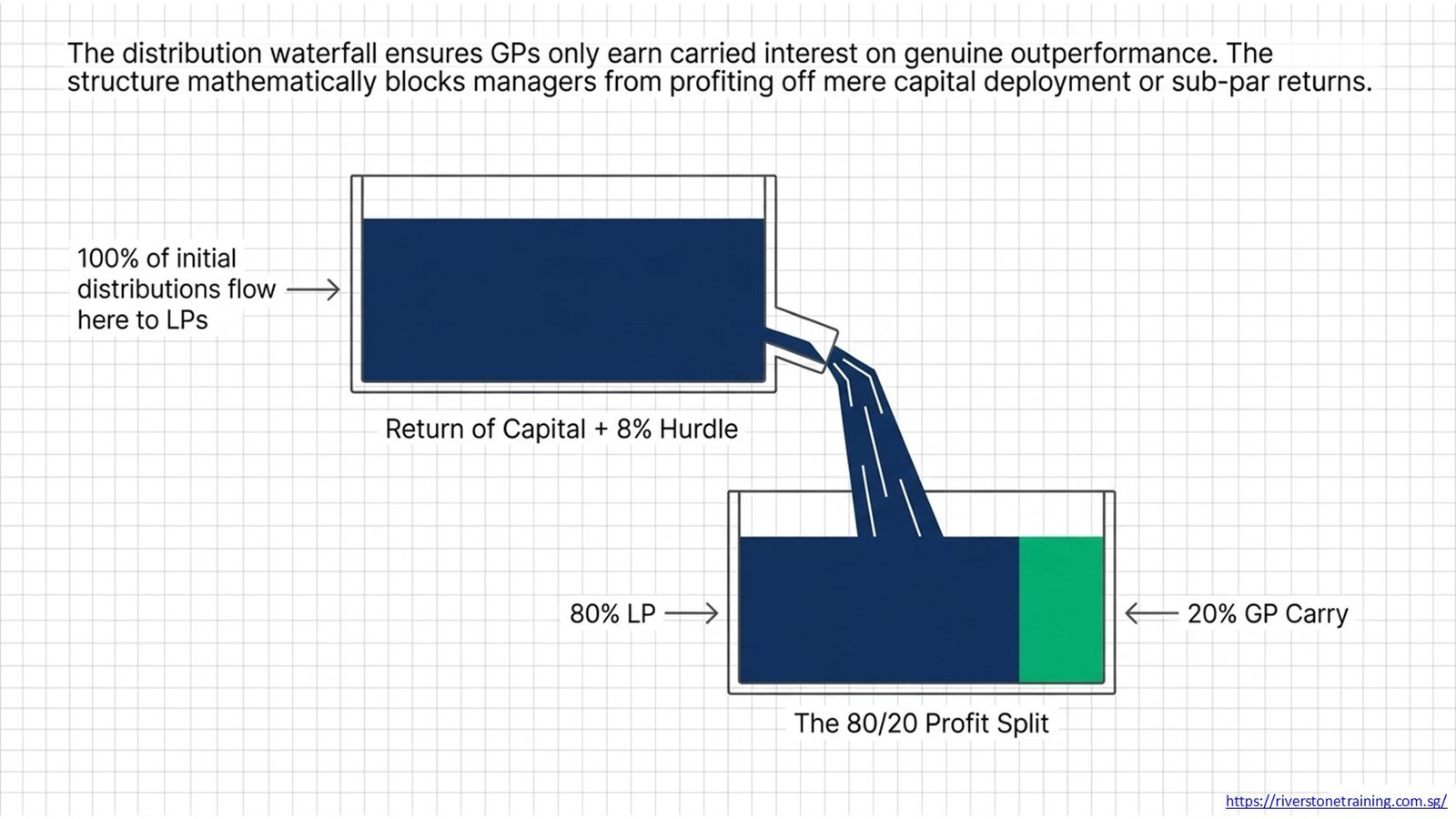

The Limited Partnership Agreement is the basic legal contract that determines all aspects of the relationship between the LP and GP. It sets forth the rules and regulations on capital commitments, management fees, carried interest economics, investment restrictions, GP removal provisions, fund term, distribution waterfalls, and GPAC governance rights.

Professionally, the LPA is not just a legal document but one that affects various aspects of fund economics, including when distributions are made, what constitutes a key-man clause, and how fund economics are calculated. When analyzing fund commitments, auditing GP compliance and structuring co-investment relationships with main fund investments, private equity professionals learn the language and the meaning of LPA terms.

How Are Management Fees and Carried Interest Structured?

Management fees, which are typically 1.5–2.0% per year on committed capital, generate revenue for the GP to help pay for staff salaries, deal costs and administrative expenses. Fees are flat no matter how well the fund performs, and gradually decline after the investment phase has ended, sometimes declining to 1.0-1.5% of invested funds at the harvest stage.

The GP performance incentive is a 20% cut of profits over the preferred return hurdle (usually 8% IRR), commonly known as “carried interest.” Carry is only paid once the LPs have gotten back their committed capital, plus any hurdle return, so that the fee structure is built to pay for outperformance and not just the deployment of capital. Clawback clauses will mean that, if the overall return of the fund falls below the hurdle level in the future, then the GPs will have to return the carry they have received in the past.

Table 3: Incentive Structure — Management Fees vs Carried Interest

| Component | Management Fee | Carried Interest |

| What It Is | Annual fee charged by GP for managing the fund | GP’s share of profits above the hurdle rate |

| Typical Rate | 1.5%–2% of committed capital p.a. | 20% of profits above the hurdle rate |

| Trigger | Charged annually regardless of fund performance | Earned only after LPs receive preferred return (8% hurdle) |

| Purpose | Covers GP operating costs — staff, research, admin | Aligns GP incentives with LP capital appreciation |

| Clawback? | No — non-refundable operational expense | Yes — GP may return carry if the fund underperforms later |

How Do Capital Commitment and Capital Call Work in Practice?

Each LP signs the LPA and makes a capital commitment (legally binding promise to provide capital when requested to do so) at fund close. The GP will keep an unfunded commitment schedule that details the amount of each LP’s commitment and the total amount of the commitment, and when issuing a capital call notice, will call down capital in proportion to that LP’s pledge.

In practice, GPs give a notice of capital call a few weeks ahead of the funding date, stating the reason for the call (such as acquiring a Portfolio Company X), the amount and the pro-rata share of the LP. Capital call calculations have to be in line with the provisions as set in the LPA, a responsibility that requires private equity operations professionals to be trained and gain experience in fund administration.

How Does the LP GP Structure Align Incentives Between Investors and Managers?

One of the most important roles of the LP–GP is that it promotes incentive alignment. The GP’s agreement guarantees that the fund managers have to invest with the LPs and share the profits and losses. When the hurdle is passed, it is only then that carried interest is paid, incentivizing the GP to create better returns, not just because they invested.

Waterfalls are also in place to ensure that GPs do not benefit from early exits compared to later exits; clawback clauses and key-man clauses also safeguard LP interests. Another alignment mechanism comes from co-investment rights, which enable the LPs to invest in selected transactions alongside the fund at a lower fee drag.

What Role Does the Management Company Play in Fund Operations?

The management company is a legal entity separate from the GP, usually a registered investment manager, that the GP employs investment professionals and where the GP receives and pays management fees and where the GP will complete regulatory requirements. It is separate from the fund and provides liability separation between the investment activities of the fund and the GP’s operating costs.

It is essential to have a clear understanding of the role of the management company in order to structure the fund, comply with regulatory requirements, and ensure tax efficiency. In Singapore, for example, the management company must be licensed under the securities laws to manage the third-party capital. Operational, compliance or investor relations fund professionals should be familiar with the interactions between the fund and LPA obligations and the management company.

Table 4: LP and GP Responsibilities and Risk Allocation

| Area | LP Responsibility | GP Responsibility |

| Capital Provision | Fund capital commitments when called | Contribute GP commitment (1–2%) |

| Investment Decisions | None — delegated entirely to GP | Full authority over deal sourcing and execution |

| Legal Liability | Limited to committed capital only | Unlimited — personally liable for fund obligations |

| Fund Governance | LPAC participation; consent on conflicts | Full fund management and reporting obligations |

| Regulatory Risk | Minimal — passive investor classification | Registered fund manager; compliance obligations |

| Downside Risk | Loss limited to capital invested | Reputational and carry clawback risk |

How Do Private Equity Professionals Use the LP-GP Structure in Deal Execution?

The LP–GP structure is essential in understanding deal execution, where size, leverage ratios, and return modelling are two major aspects of the transaction. Before investing fund capital, teams should verify that the investment they are proposing adheres to the concentration limits, sector focus, geography, and co-investment terms restrictions in the LPA.

Analysts break down investment economics (gross IRR, net IRR, MOIC and DPI) at the fund level to illustrate a return’s journey through the return distribution waterfall to LPs and GP carry pool. This involves being able to become fluent with the distribution workflow and fee modeling, as well as modelling capital accounts. These skills are fundamental to the private equity industry and are developed in the structured private equity training courses, which focus on the mechanics of the private equity industry and on financial analysis of the deals.

What Risks and Responsibilities Do LPs and GPs Each Carry?

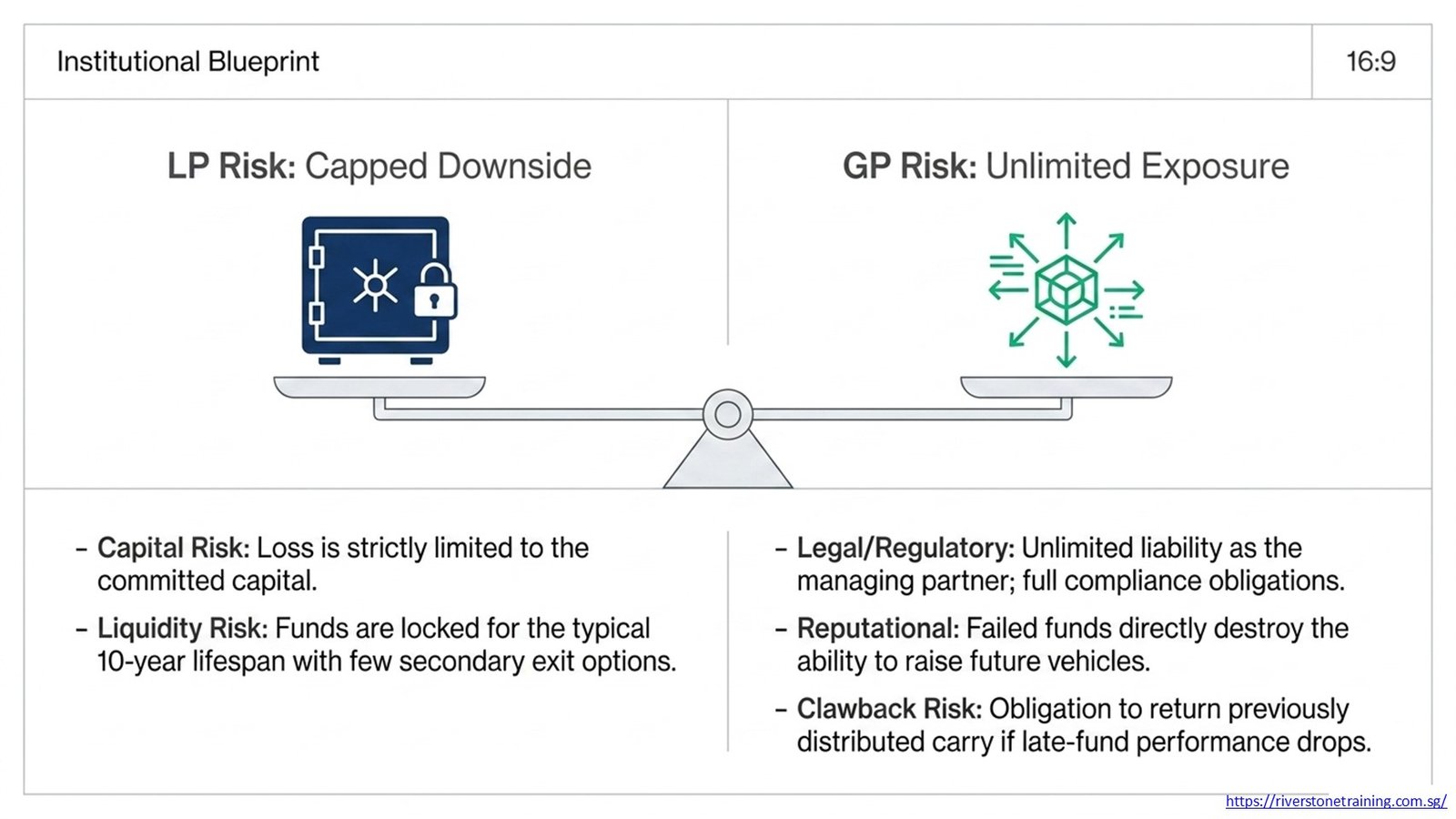

LPs are exposed to capital risk, which refers to the possibility of losing their capital if the investments of the fund do not match their expectations, but their loss can be limited to the amount of capital that they invested in the fund. Additionally, LPs are exposed to liquidity risk because private equity money is only available in the fund for the fund’s lifespan (typically 10 years) and there are few secondary market exit options. Through portfolio construction by vintage and strategy, institutional LPs minimise this.

GPs have three types of risks – reputational, operational and legal. The GP, as the manager of the fund, accepts responsibility for the fund, on its investment decisions, fund obligations, and regulatory compliance. If a fund is unsuccessful, it will hurt the GP’s ability to bring up future vehicles. Carried interest clawbacks are a significant risk that GPs must be able to manage because they may have to pay back millions in carry previously distributed by the fund if performance in later years drops below expectations.

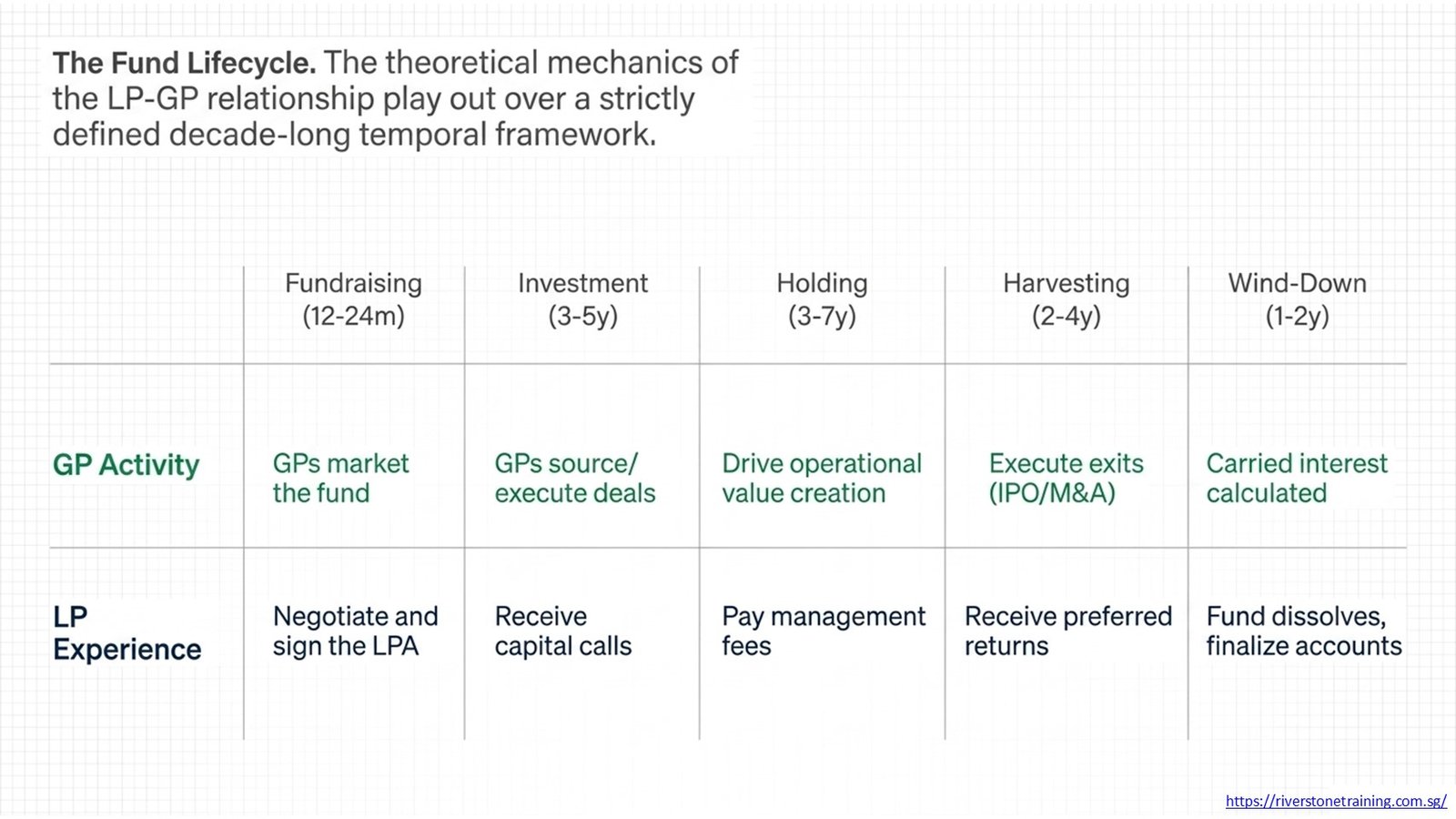

Table 5: Private Equity Fund Lifecycle

| Phase | Duration | Key Activity |

| Fundraising | 12–24 months | GP markets fund to LPs; LPA negotiated and signed; capital commitments collected |

| Investment Period | 3–5 years | GP sources, evaluates, and executes deals; capital is called from LPs as investments close |

| Holding Period | 3–7 years | GP manages portfolio companies, drives operational improvements and value creation |

| Harvesting | 2–4 years | GP executes exits via trade sale, secondary, or IPO; proceeds returned to LPs |

| Wind-Down | 1–2 years | Final distributions made; carried interest calculated; fund closed and entities dissolved |

How Is the LP GP Structure Covered in a Private Equity Professional Course?

A structured private equity professional course provides participants with an understanding of the mechanics of LPs and GPs not only as legal theory but as the structure that guides investment decisions, capital flows, and incentivization in real money. Participants will learn how to read and understand provisions in the LPA, model management fees and carry economics, and how to analyse fund performance from both LP and GP perspectives.

Courses for investment professionals encompass the entire lifecycle of a fund, ranging from raising capital to capital calls, to dealing execution, fund management and exit distribution. After private equity training, finance professionals, analysts, fund administrators and institutional investors are equipped with the structural information to analyse fund commitments, assess GP track record and model accurately on the economics of the fund level.

Conclusion

The private equity LP – GP structure is the operational and legal structure of all private equity funds. It outlines the process of raising capital from institutional investors, the process of delegating investment authority to a specialist manager, how fees are calculated, how performance incentives are calculated, and how profits are allocated throughout the life of the fund. This is the path for all facets of private equity – deal sourcing, fund performance and analysis, and more.

Whether you’re an individual entering the private equity world or simply want to expand your investment knowledge, understanding LP–GP mechanics is essential. The deeper you delve into the details of capital calls, LPA terms, distribution waterfalls, and incentive alignment, the better you can make investment decisions, assess a fund, and communicate with stakeholders. Whether you’re an analyst modelling fund economics, an investor evaluating GP commitments, or a finance professional making their way into the private equity space, a rigorous private equity professional course offers the structure to develop these skills with precision.