The private equity fund economics are based on management fees, carried interest and waterfall distribution structures. These mechanisms outline the allocation of capital, profits and returns to fund managers (GPs) vs investors (LPs).

What Are Private Equity Fund Economics?

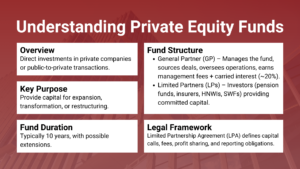

The overall financial framework that regulates the interaction between a fund manager and the investor is referred to as private equity fund economics. It includes the mechanism by which a Fund makes returns, the distribution of the returns, and the compensation of the manager during the life of the Fund.

A private equity firm is generally incorporated as a limited partnership. The GP is in charge of the fund and decides where to invest, and the LPs invest money and get a return. That is, value is created and distributed based on the economic terms found in the fund’s limited partnership agreement (LPA).

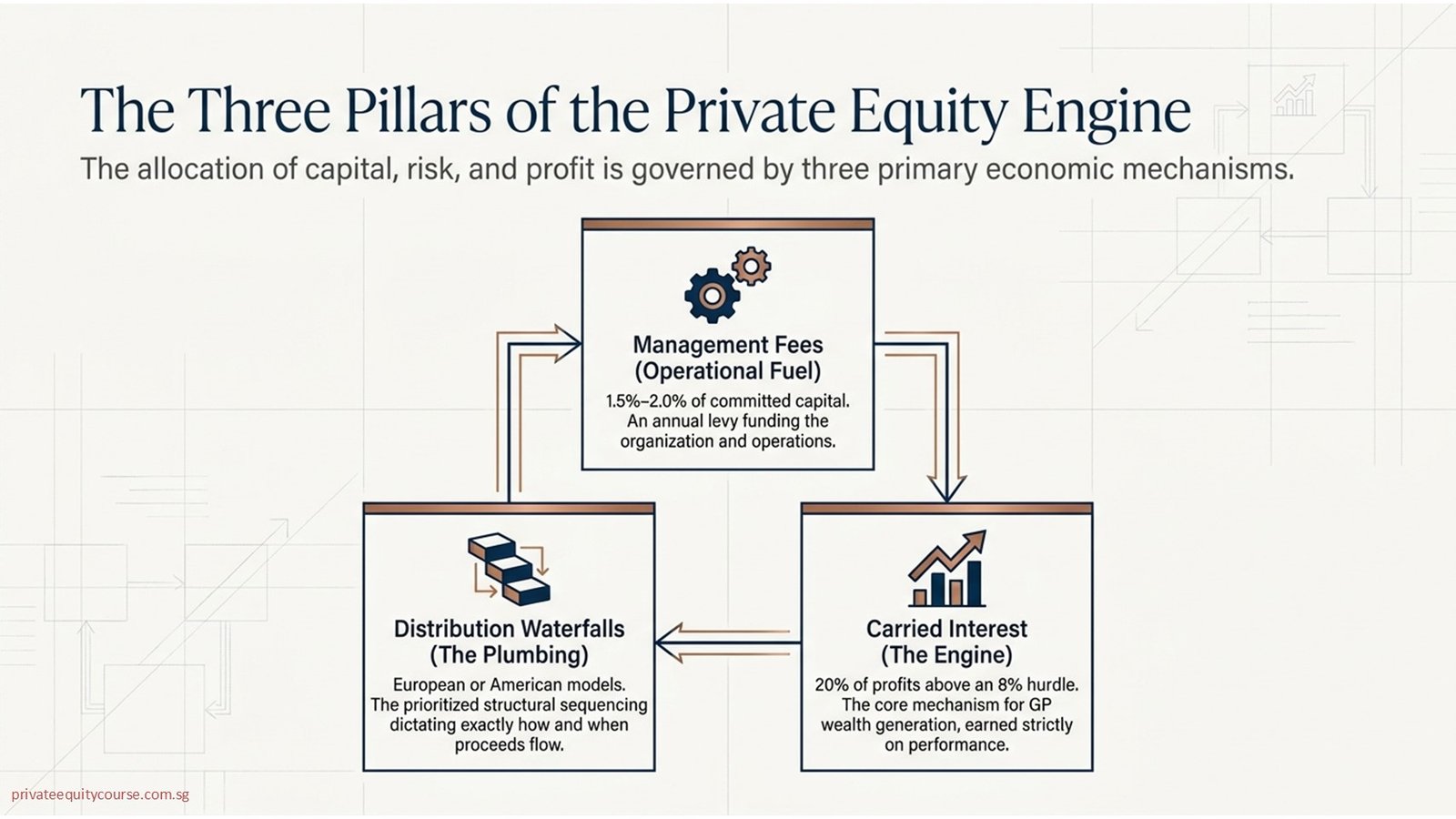

The three principles of private equity fund economics are management fees (long-term operating fees), carried interest (performance-based fees) and distribution waterfalls (how and when proceeds are distributed). All of these components make up the incentive framework of the fund and directly influence the fund’s net returns to investors.

To get a basic idea of how these economic terms fit into the overall partnership framework, it is helpful to first have a basic idea of the

It is helpful to first understand the private equity fund structure basics (GP and LP, fund life cycle stages, and the mechanics of a capital call) in order to understand how these economic terms fit into the partnership structure.

The table below summarizes the key components of private equity fund economics at a glance:

| Component | Definition | Typical Terms | Who Benefits |

| Management Fee | An annual fee levied by the GP for the cost of running the organization. | 1.5%–2.0% of committed capital | GP (fund manager) |

| Carried Interest | Profits above a minimum level are shared by GP. | 20% of profits above 8% hurdle | GP (performance reward) |

| Preferred Return (Hurdle) | The minimum return LPs must be returned before GP receives the carry. | 8% per annum (IRR-based) | LPs (investor protection) |

| Distribution Waterfall | The order and criteria in which assets are distributed | European or American structure | Determines GP vs LP split |

| GP Clawback | Mechanism requiring GP to return excess carry received | Triggered if the overall fund underperforms | LPs (capital protection) |

How Do Management Fees Work in Private Equity Funds?

The biggest source of operating income for a private equity fund manager for the fund’s life is management fees. They are paid on a yearly basis and are meant to fund the team salary, running the office, sourcing deals, legal fees and continued monitoring of the portfolio.

The management fee is 2% per year on committed capital until the end of the investment period, usually the first 5 years of the fund. Typically, once the investment period has passed, the fee base would transition to net invested capital or the fair market value of the portfolio, thereby alleviating the burden on investors as the portfolio grows.

Management fees are not a performance-based instrument; they are paid regardless of fund performance. This is a significant difference from carried interest. There has been criticism that the GP might see returns from poor-performing funds due to high management fees, and so fee terms have become negotiable between institutional LPs and GPs.

Management Fee Structure Across Fund Life Cycle:

| Fund Phase | Fee Base | Typical Fee Rate | Rationale |

| Investment Period (Years 1–5) | Committed Capital | 1.5% – 2.0% | Covers active deal sourcing and execution |

| Post-Investment Period (Years 6–10) | Net Invested Capital | 1.0% – 1.5% | Reflects reduced workload as portfolio matures |

| Extension Period (if applicable) | Remaining Invested Capital | 0.5% – 1.0% | Minimal fee for winding down activities |

Some fund managers have also been imposing monitoring fees, transaction fees and deal fees at the level of the portfolio company. However, more and more, a percentage of these fees (sometimes up to 100%) would be offset against the management fee, meaning that the net fees to LPs would be lower.

What Is Carried Interest and How Does It Work?

The compensation of GP on the profitability of the fund is known as carried interest, or simply ‘carry’. It is the most important mechanism for wealth generation for the private equity professionals and it directly links the incentives of the GP with the ability to generate a strong return for the LPs.

Carry is generally 20% of profits over the threshold for the preferred return, but can be as high as 25% or more in the case of high-quality funds. Once LPs have been paid back their invested capital together with the agreed preferred return (also called the “hurdle rate”), which is typically an 8% per annum compounded quarterly, Carry is earned.

No guarantees of carried interest. If the fund does not meet the hurdle rate, then the GP does not receive any carry. Such a set-up is a good incentive for the GP to push the fund to perform rather than just invest.

Carried Interest Calculation Example:

| Item | Amount (USD) |

| LP Committed Capital | $100,000,000 |

| Preferred Return (8% p.a. over 5 years) | $46,933,000 (compounded) |

| Total Amount Before Carry | $146,933,000 |

| Total Fund Proceeds at Exit | $200,000,000 |

| Profit Above Preferred Return | $53,067,000 |

| GP Carried Interest (20% of Profit) | $10,613,400 |

| LP Net Distribution | $189,386,600 |

The typical terms of a carry include a vesting schedule and clawback. This clawback is included in the event that a GP makes high returns when selling out the investment early, but the overall fund returns under the LPs’ expectations.

A strict methodology is necessary for the valuation of portfolio companies during the time of carry calculation. Funds subject to accounting standards have to apply

At the time of carry calculation, there should be a proper valuation methodology for the portfolio companies. Funds subject to accounting standards must apply fair value measurement under IFRS 13, which prescribes how assets and liabilities should be measured at fair value using market-based inputs, ensuring that unrealised gains used in carry calculations are defensible and consistent.

How Do Waterfall Models Distribute Returns in Private Equity?

The sequence and priority of payment of investment proceeds to LPs and GP are determined by a distribution waterfall, which is a contractual agreement. The waterfall determines who will be paid first, who will be paid less, and what will be the point of GP’s involvement in the profits.

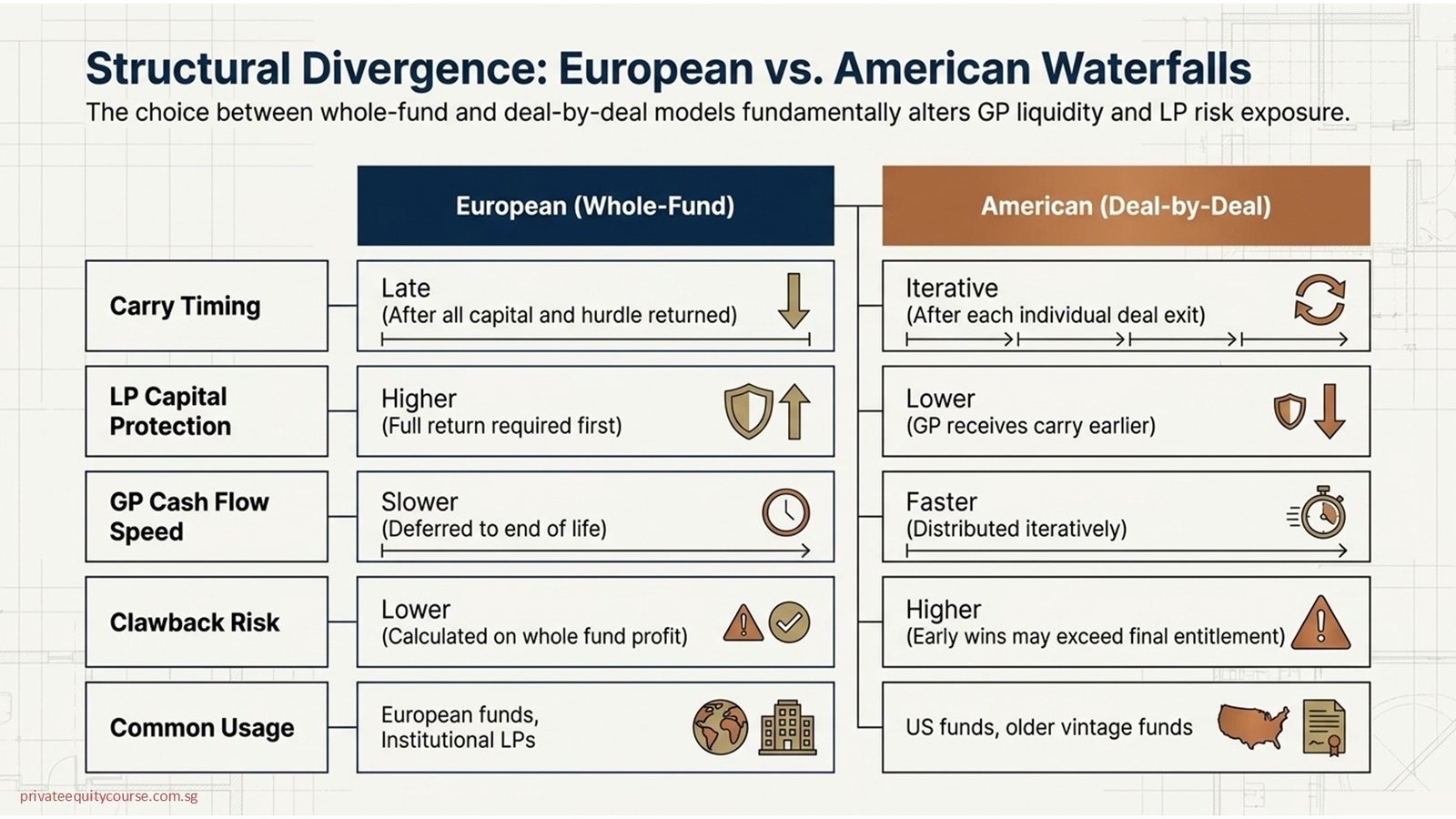

Private equity firms typically have two types of waterfall arrangements – a European (whole-fund) waterfall and an American (deal-by-deal) waterfall. They each have significant material implications for GP carry timing and level of LP capital protection.

European vs. American Waterfall — Key Differences:

| Feature | European (Whole-Fund) | American (Deal-by-Deal) |

| Carry Timing | The value of the LP capital and hurdle returned after all. | After each individual deal exit |

| LP Protection | Higher — full capital return required first | Lower — GP receives carry earlier |

| GP Cash Flow | Slower — carry deferred until late in fund life | Faster — carry distributed deal-by-deal |

| Clawback Risk | Lower — carry only paid on the overall fund profit | Higher — early carry may exceed final entitlement |

| Common Usage | European funds, institutional LPs | US funds, especially older vintage funds |

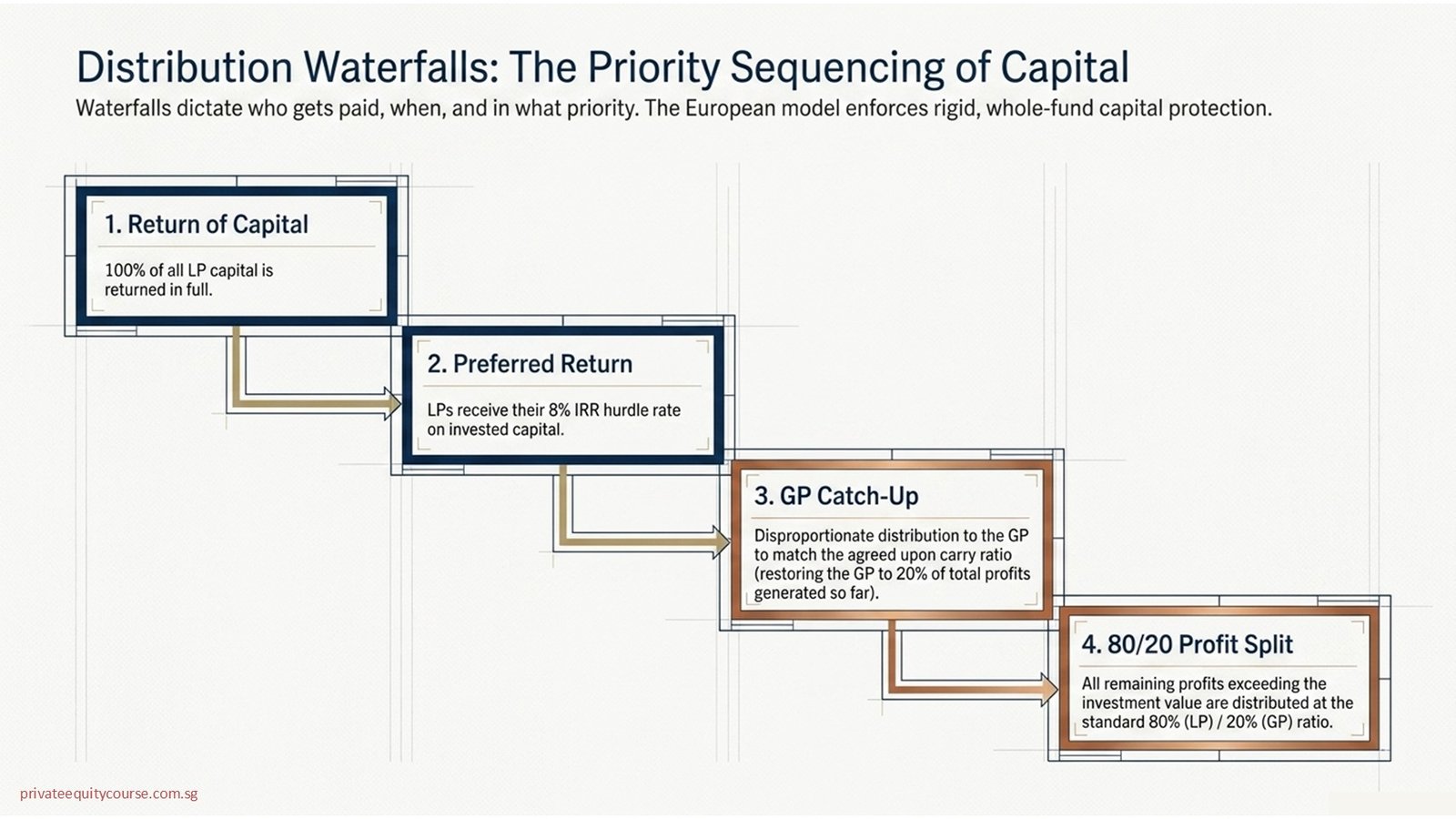

European Waterfall Structure:

A European waterfall is a very rigid sequence. One, all of the capital of LP is returned in full. Secondly, LPs get their preferred return (usually 8% IRR). Third, a catch-up payment is made to the GP, a distribution that is not proportional, which is intended to ensure that the GP’s total distribution equals the agreed carry. Lastly, any profits that exceed the value of the investment are distributed based on the GP/LP ratio, which is typically 20/80.

American Waterfall Structure:

The American waterfall gives the GP a carry for every deal that it exits, if it has returned the preferred return and invested capital. This is more advantageous from a GP cash flow point of view, but is more complicated in terms of clawback due to the added complexity, and if there is no escrow in place to safeguard the LPs.

How Are Private Equity Funds Structured Around These Economic Terms?

In addition to the economic terms mentioned above, management fees, carried interest, and waterfalls are not standalone concepts. They are governed by a legal framework and structural rules that regulate the functioning of the fund from its inception to its termination.

The LPA is the governing agreement that lays out every aspect of the economic terms, decision-making power, and investor protections. Some of the main features are the calculations of the fees, carry rates, hurdle rate, mechanics of distribution waterfalls, investment period, fund life, extension options, and GP removal rights.

The size and type of the fund have a significant impact on economic terms. Large funds with proven track records may have better carry rates and fee sizes, while newer managers might have more attractive terms to draw institutional investment.

Summary of Key Fund Economic Terms and Their Function:

| Economic Term | Governed By | Typical Range | Primary Function |

| Management Fee | LPA — Fee Section | 1.5%–2.0% p.a. | GP operational income |

| Preferred Return / Hurdle Rate | LPA — Distribution Waterfall | 7%–8% IRR | LP minimum return protection |

| Carried Interest | LPA — Carry Section | 20% (top funds: 25%+) | GP performance incentive |

| GP Catch-Up | LPA — Waterfall | Full or partial catch-up | Restores GP/LP profit ratio |

| Clawback | LPA — Clawback Clause | 100% of excess carry | LP capital recovery mechanism |

| GP Commitment | LPA — GP Commitment | 1%–3% of fund size | GP skin-in-the-game alignment |

| Fund Life | LPA — Duration | 10 years (+ 1–2 yr extensions) | Investment and harvesting period |

These terms interact to define the overall economic benefit to LPs and the incentive to the GP. Sophisticated institutional investors such as pension funds, sovereign wealth funds, and endowments review LPAs in detail and may discuss changes to the typical LPA terms prior to the investment of capital.

What Should Finance Professionals Know When Evaluating Private Equity Fund Economics?

The economic terms of the fund are not just an academic discussion, but they can have an impact on the net-of-fee performance, risk levels, and interests of both the GP and LPs.

An analytical issue that is most relevant is that of the net IRR to LPs after management fees, carried interest, and other expenses. If the arrangements of the fees are not favourable, a fund can have high gross returns, but poor net returns. LPs should simulate several different scenarios (base case, downside, and upside) and evaluate how the waterfall will be affected by each of those return profiles.

Questions finance professionals should consider asking when looking at fund terms are: When does GP get to “earn his carry”? Which is the fall of Europe or America? What is the catch-up system? Does the contract have a clawback, and how is it protected? What are the offsets available to the management fees?

The concept of co-investment rights, preferential share classes, and the marriage of economic and other hybrid structures have complicated the economics of private equity funds further. Understanding these mechanisms is crucial for those involved in fund structuring, investor relations, or portfolio management to navigate the asset class effectively.

Conclusion of Private Equity Fund Economics

Private equity fund economics are a very exact and interconnected system. The key components to management fees are operational income for the GP, carried interest to reward performance and align interests, and waterfall models to determine how and when the profits are distributed between LPs and GPs. The relationship manifested at the heart of any private equity fund is governed by detailed contractual provisions in the LPA, each of which is an important factor.

It is important for finance professionals, both on the GP end of the fund structuring and on the LP end of the investment fund to be well-versed on these mechanics. The distinction between a European and American waterfall, between a partial and full catch-up, or between the clawback exposure and the clawback realized has a material impact on actual returns and risk management outcomes.

The understanding of fund economics and their application will continue to be a key skill for anyone working in the private equity asset class, as the growth of the asset class continues to gain institutional interest worldwide.