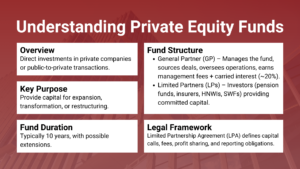

Private Equity Fund Structure Explained: GP, LP, and Fund Life Cycle

Private equity (PE) is a dynamic investment approach that allows investors to take part in the growth and transformation of private companies. Both investors and companies looking for capital to grow have a strong need to understand the structure of a private equity fund structure explained for investors and startups Singapore. Greatly different from the traditional investment funds, PE funds are regulated in a well-defined structure that reconciles decision-making, capital commitment and risk management. Central to this structure are General Partners (GPs), Limited Partners (LPs), and a well-defined fund life-cycle representing the integration of important contributors to successful investment performance. Private equity fund is not merely a capital pool. Risks inherent in this partnership between the asset managers, recposing the producers of capital investments, and the capital providers, who deploy the capital demanded for the investments. The structure of the fund determines how decisions are made, how profits are distributed and risks are allocated. Furthermore, knowledge of the fund life cycle can help investors and companies in the portfolio to forecast the timing of investment, exit, and return of their responsibilities. In this article, the private equity structures and the main roles assigned to different parties like GPs and LPs, in addition to the fact that a PE fund has a life cycle with distinct stages, will be explained in detail.