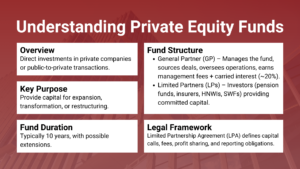

Private Equity Modeling Test Prep

To enter into the industry as a private equity or to rise to the top within the industry, it takes more than a good resume. Companies subject potential employees to rigorous financial modeling exams to determine the way the candidate thinks under pressure, how he or she organizes complicated problems, and whether or not he/she understands the mechanics behind investment returns. The process of the private equity investment may be abstract to many candidates, until they find themselves in front of a blank excel sheet with a three hour clock running. It is not an option, then, preparation is what will make the difference between getting to the final round and getting a polite rejection email.

The article is targeted at junior to mid-level finance professionals such as analysts, associates, and former investment banking, consulting, or corporate finance professionals who would like to tackle modeling tests with precision and confidence. Regardless of whether you are taking a course in a private equity modeling test, or are teaching yourself, the paradigms and insights here will enable you to work more quickly, think more accurately, and present your work in a manner that will appeal to investment professionals.

It discusses the structure of a properly developed leverage buyout (LBO) model, the five steps every applicant needs to take, the pitfalls which can take otherwise good performers off track and real-life examples based on the actual types of deals. It also deals with what companies are actually assessing that is, hardly about perfection, and nearly always about organized thinking, good assumptions and what you can say in a discussion to justify your analysis.

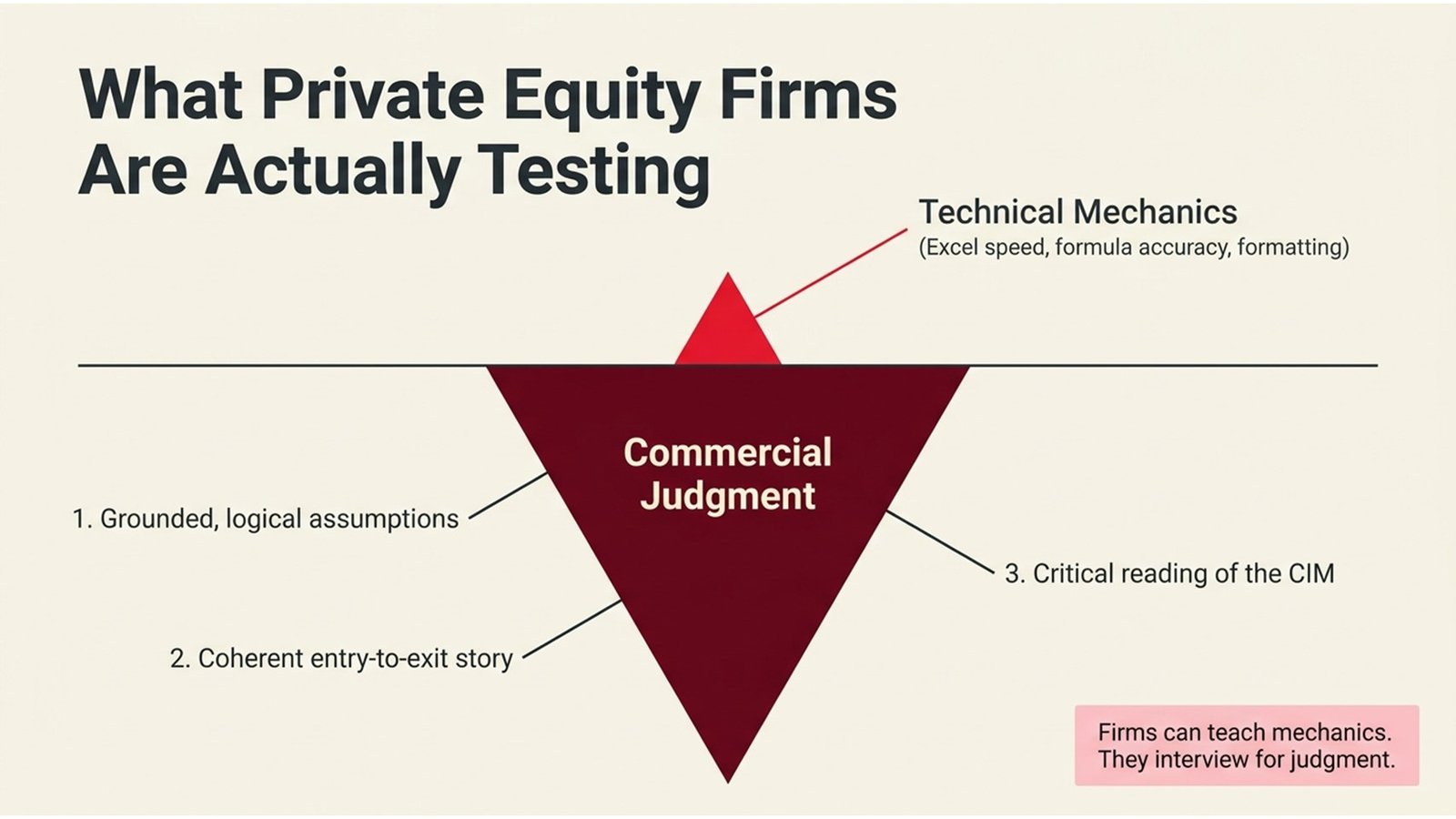

What Private Equity Firms Are Actually Testing

The majority of candidates believe that the modeling test is all technical – a test of the speed and accuracy of the formulas in Excel. Although they are important, experienced partners and associates with submissions are mostly posing another group of questions: Does this individual know the business? Is the reasoning based on logic? Does the model make a sense of the entry to exit? It is these questions that define what the private equity investment process, and companies will be willing to learn that its future employees share similar worldviews.

The candidate who constructs a mechanically correct model of LBO but bases his revenue assumptions on assumptions that are not consistent with those of the industry will do worse than the candidate who constructs a model with a minor formatting mistake but which exhibits a clear commercial point of view. The testing environment is set up to be a simulated real deal, usually a Confidential Information Memorandum (CIM) in the case of a fictitious or anonymized company and candidates are given the expectation that they will read critically, rather than simply dump the data into their model.

An insight into this framing is important as it alters your preparation process. It is worth taking private equity financial modeling course work but the most successful applicants supplement this with reading industry reports, CIMs of previous deals and announcements of their portfolio companies. This is aimed at building judgment and not only mechanics. The latter can be taught by firms; they are interviewing about the former.

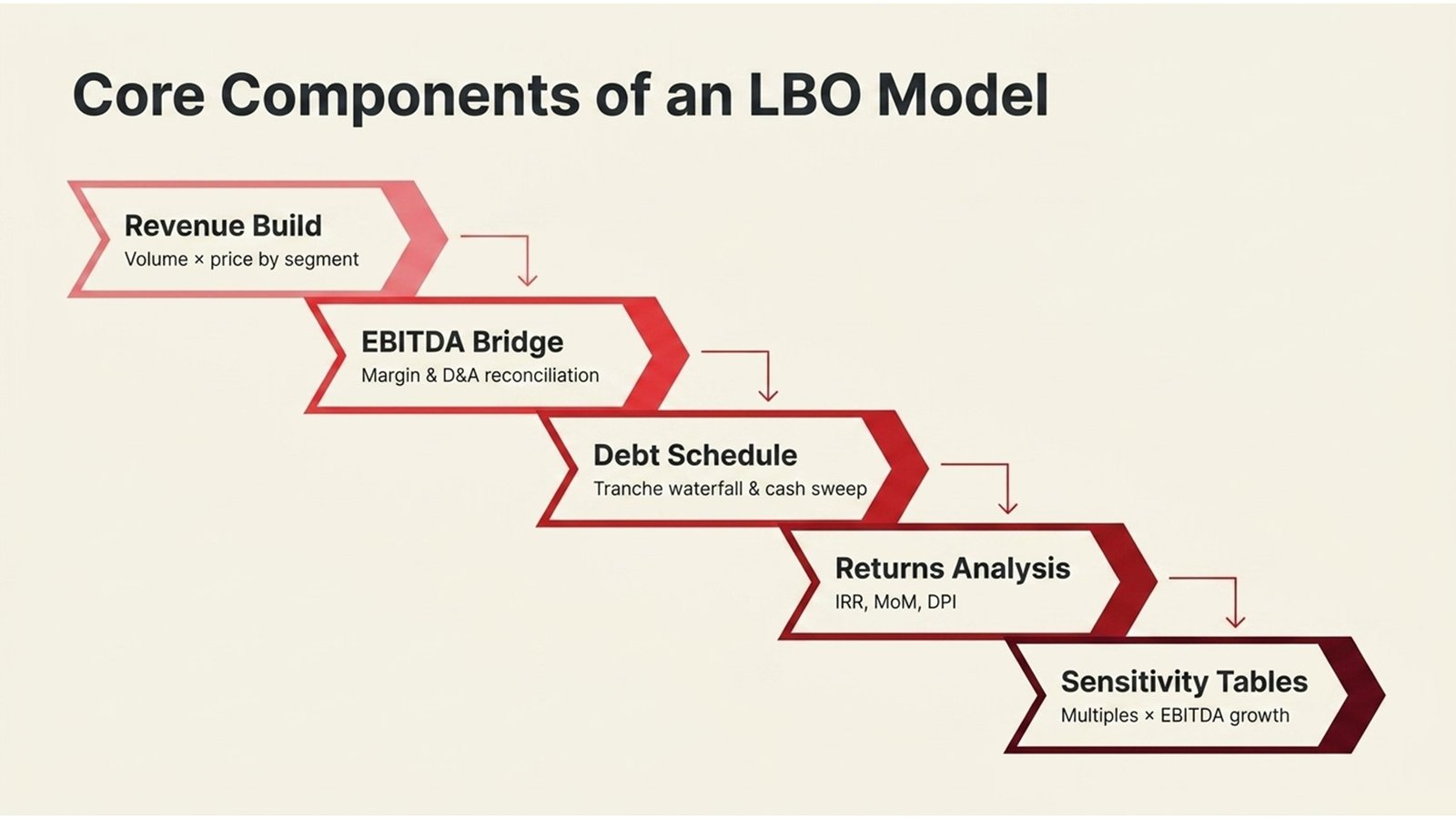

Core Components of an LBO Model

A model LBO is well designed to have a logical architecture that would replicate the manner in which a firm conducts a deal. It is based on five mutually related elements: the operating model, the transaction structure, the debt schedule, the returns analysis and the sensitivity framework. It is much easier when candidates can comprehend how these parts interrelate, and the reasons behind it to create in a way that is highly efficient in a time-constrained environment.

Commercial judgment can be most evident in the operating model. Beginning with historical financials, the candidate needs to create a plausible revenue projection, create a bridge of margins explaining how EBITDA changes over the holding period, and convert operating profit into free cash flow by making CapEx and working capital assumptions. Every individual line item must be justifiable – not merely mathematically, but strategically. In case a course in private equity modeling that you have attended does not adequately devote time to assumption-setting rationale, this is a gap that can be filled in by looking at further case studies.

A reference summary of the five core model components, the major outputs that each component must yield and the most common mistakes made at each stage have been provided below. Candidates that absorb this structure will be in a position to work very fast and not lose their directions during the test.

Table 1: LBO Model Component Reference

| Model Component | What It Covers | Common Pitfall |

| Revenue Build | Volume × price assumptions by segment | Dependence on management forecasts. |

| EBITDA Bridge | Gross margin, SG&A, D&A reconciliation | Combining repeat vs. non-repeat. |

| Debt Schedule | Tranche waterfall, PIK, cash interest | Ignoring sweep mechanics |

| Returns Analysis | IRR, MoM, DPI, RVPI | Mixing up equity vs. enterprise returns. |

| Sensitivity Tables | Entry multiple × exit multiple × EBITDA growth | Choosing unrealistic range of scenarios. |

Five Key Steps to Nail the Modeling Test

Good results on a modeling test are no mere coincidence. The successful candidates always go through a systematic process that involves time management, logic and allows them to review. This is the five steps that the most successful test-takers use, no matter what type of deal or industry it is.

- Read the CIM before opening Excel

Take 15-20 minutes to read the information pack. Determine revenue model (recurring vs. transactional, product vs. service), the most important cost drivers and the said growth strategy by the management. Mark anything that is positive or that needs a normalization change. This initial cost is a time saving that will pay off in the future and avoidance of expensive assumption errors.

- Build a clean tab architecture first

You will want to have your worksheet tabs arranged before you can enter your single formula: Cover, Assumptions, Income Statement, Balance Sheet, Cash Flow, Debt Schedule, Returns, and Sensitivity. The logical structure simplifies the process of reviewing the model – by you and by the evaluators. This is why the step is given special focus in many of the courses in financial modeling in private equity because it is in situations where candidates feel under pressure that they overlook it.

- Drive everything from a centralized assumptions page

All the important inputs, including growth rates of revenue and margin, CapEx relative to revenue and entry/exit multiples, debt terms, etc. should reside in a single tab. Numbers embedded in formulas are the most prevalent and cause of errors and virtually impossible to scenario analyze. Assign each assumption a unit and source/rationale.

- Layer in the debt schedule and returns with care

After you have filled in the operating model, construct the debt schedule to indicate the capital structure of transaction: senior secured, unitranche, mezzanine or whatever is being mentioned in the prompt. Find the necessary amortization and cash sweep. Construct equity bridge: then construct equity bridge between entry and exit, compute IRR and money-on-money (MoM) multiple and make a sensitivity table indicating returns under various combinations of exit multiples and EBITDA growth.

- Audit and sense-check before submitting

Allot the last 15-20 minutes time to review. Check balances on the balance sheet, cash flow is linked to the change in cash on the balance sheet and IRR numbers are reasonable to the type of deal. Perform some sanity checks: is 3.0x MoM over 5 years suggesting an approximate IRR of 25%? Is its revenue growth comparable to those that are achieved by similar companies? These tests show the type of business acumen that companies are seeking.

Process Flow 1: PE Investment Process — From Sourcing to Value Creation

| Stage 1 | Stage 2 | Stage 3 | Stage 4 | Stage 5 | Stage 6 |

| Deal Sourcing | Initial Screening | Due Diligence | IC Approval | Signing & Closing | Value Creation |

| Advisors, Auctions, proprietary networks. | Sector fit, size, quality of EBITDA. | Financial, legal, commercial, ops. | Investment committee memo & vote. | Legal close, debt funding, SPA. | Exit prep, bolt-ons, 100 day plan. |

Process Flow 2: Modeling Test Execution — Five-Step Workflow

| Step 1 | Step 2 | Step 3 | Step 4 | Step 5 |

| Read CIM / Info Pack | Set Up Architecture | Build Operating Model | Layer Debt & Returns | Sense Check & Present |

| Flag key drivers, type of revenue model, profile of margins | Cover, Assumptions, IS, BS, CF, Debt, Returns tabs | Revenue → EBITDA → CapEx → free cash flow | The tranche waterfall, IRR, MoM, sensitivity table. | Check BS balances, respond to questions about investment thesis. |

Real-World Deal Types and What They Test

Modeling tests are not often abstract. They are pegged to familiar deal archetypes, and familiarity with the peculiarities of any given type can guide candidates to get their assumptions rapidly in tune. The most popular three archetypes to be applied in tests are software/SaaS buyout, industrials or business services LBO, and consumer/retail acquisition.

Take a software company whose recurrence is 85, and EBITDA is 30 percent- recurrence and EBITDA profile which is typical in take-privates. The revenue line modeling here is not so difficult (it is a fairly predictable challenge) but the R&D and sales expenditure needed to nurture the growth. Any candidate that projects flat headcount and projects a 20 percent ARR growth will instantly sound alarm bells. The discipline of the real private equity investment process requires consideration of the actual cost of growing a business and not the appearance of the P&L at the exit multiple. In a real-life parallel, when European PE firms considered mid-market SaaS businesses in the 2021 to 2022 cycle, they were most able to model the cost of growth versus the value of retaining ARR, and most credible investment theses was associated with the latter.

In comparison, an industrials or business services LBO generally has lower margins (8 to 15% EBITDA), a high working capital intensity and a value creation thesis that relies on operational improvement or bolt-on acquisitions as opposed to organic growth itself. The modeling test here requires a strict working capital plan, CapEx assumptions that are clear between maintenance and growth expenditures and how procurement savings or pricing efforts can be passed through to EBITDA. These are the very skills that have been trained in well-developed private equity financial modeling courses where case studies are based on the specific industry but not on a template.

Challenges, Mistakes, and Lessons from the Test Room

Making predictable mistakes even well prepared candidates make. One of the most valuable kinds of preparation is to know in advance what these mistakes are, and why they take place. The most regular trend in terms of test submissions is the speed vs. structure trade-off: candidates who hurry up to create outputs without a logical architecture nearly always create models that are more difficult to audit, more easily broken and harder to justify during the debrief interview.

The other challenge that is commonly witnessed is the over reliance on the CIM projections itself. The financials in management cases in a CIM are nearly always optimistic- that is their role in a sale process. Older candidates take management projections as a ceiling, rather than a bottom case, and construct their own bottom-up revenue projection and see how far it differs with what management has purported it to be. The fact that the two cases are different and can be explained by something is what makes an otherwise technically competent model a truly remarkable work of analysis.

The following table summarizes the four most frequent modeling errors observed when submitting tests and the solutions. This should be a pre-submission checklist to the candidates preparing with a private equity modeling test course.

Table 2: Common Modeling Mistakes and Remedies

| Mistake | Why It Matters | How to Fix It |

| Hard-coding assumptions | Breaks of models on scenario analysis. | Make use of a special assumptions tab. |

| Circular references unflagged | Excel can do inaccurate calculation. | Allow calculating in an iterative way. |

| Ignoring working capital | Excessive cash flow on exit. | Develop clear NWC timetable. |

| No sanity checks | Errors compound silently | Add rows to check: BS balance, cash ties. |

In addition to technical errors, during the debrief conversation, which usually follows the submission, most candidates forfeit some of the ground that they had gained during the modeling phase. Questions that firms would follow up on include: What was your revenue assumption? or What would it take to have this deal be a 25% IRR? These are not questions to get the candidates stumbling, they are meant to get to know how the candidate thinks. Candidates who are able to describe the reasoning behind each assumption, even approximate reasoning, will always do better than those who constructed a more elaborated model, which they are unable to describe.

Conclusion: Turning Preparation into Performance

By nature, the tests of the private equity models are difficult. They squeeze the amount of real work one would have in a week into three or four hours and challenge applicants to be technically precise, commercially astute, and articulate at the same time. The positive thing is that all this set of skills can be learnt and the difference between the potential and the prepared candidate is not as narrow as most people may think.

A number of practical lessons can be derived out of all that was discussed in this paper. To start with, invest in structured training: a good course in private equity modeling tests based on realistic CIMs and case studies in specific industries will get you over your learning curve in a much shorter time. A generic DCF training is not an appropriate training to be taken in the subtle requirements of an LBO test. Second, construct your model structure prior to your initial formula — you cannot spend too long on structure. Third, you always need to put your assumptions at the center and not with numbers alone but with logic.

Fourth, research real life prototypes. The process of the private equity investment is not a one-size-fits-all approach – a software acquisition, an industrials carve-out and a consumer brand acquisition all require different modeling intuitions. The greater number of deal types you have gone through the more confident and efficient you will be in the testing circumstances. Fifth, rehearse. Record a discussion of your model aloud and practise answering the most difficult questions regarding your assumptions, and make sure that you can justify every number with no less than one sentence of reasoning.

Lastly, do not rule out the importance of the use of a private equity financial modeling courses with mentor feedback or live feedback. It is tough to be objective in reading your own work when under pressure. The quickest method of uncovering blind spots that practice tests will never tell you about is to have an experienced practitioner go through what you produce, and pose probing questions. The candidates that always do best are not always the ones that know most about money, but rather those who have been trained most systematically, who know what it is that is being tested, and who have taken the process as a profession to be learned.