Buy-and-Build Add-On Acquisitions

The buy-and-build private equity strategy is one of the most dynamic and action-packed strategies that private equity firms use to achieve higher returns. This is a strategy of buying an initial platform business – usually a less consolidated industry – and building up over time with smaller companies. When done right, the outcome is a bigger, more seamless business with more robust margins, market reach, and stronger exit multiples than the businesses could have achieved on their own.

As the buy-and-build trend gains momentum, it is essential for junior and mid-level buy-and-sell advisory, M&A, corporate development, and fund management professionals to understand how buy-and-build strategies work. Today, these strategies comprise a substantial share of deal volume around the world, and those who can provide value to the platform selection, add-on sourcing, integration management and performance tracking efforts are always in demand.

This article offers an insightful and hands-on analysis of the buy-and-build model: what it entails, how it generates value and where it typically goes wrong. It uses real-life examples and frameworks to explain not only the theory but also how it is implemented in practice, to illustrate the implementation of private equity value creation strategies that are key to this. It explores along the way the crucial function that the value of deals in the structuring phase serves in making individual deals viable and collectively accretive.

Understanding the Buy-and-Build Model

The buy-and-build private equity strategy ultimately takes advantage of the following economic phenomenon: valuation arbitrage. More fragmented industries generally have lower EBITDA multiples for smaller businesses compared to larger, consolidated businesses. A private equity firm can buy an operating platform business at say 7 times EBITDA, attach a number of smaller add-ons at 4 to 6 times EBITDA and then exit the combined business at 9 to 10 times EBITDA — getting a lot of return on multiple expansion, without considering organic growth or efficiency in operations.

Because the strategy is most naturally applicable to industries in which no one has gained dominant scale, local customer relationships, and standard operational processes across sites or divisions. Over the last decade, there has been a significant amount of buy and build activity across a variety of sectors, including veterinary services, dental, industrial services, specialty chemicals, waste management and software services. The rationale is the same in all of these industries: fragmentation opens a door, consolidation generates value and good integration keeps it open.

It is crucial for the buy-and-build private equity strategy to be able to differentiate from opportunistic bolt-on acquisitions. In a genuine “buy and build”, the add-on program is considered right from the beginning and part of the investment case. The platform business is chosen because it is expected to become a core business for further acquisitions, it is well-managed, has a scalable operating model, and will have the financial capabilities to integrate and absorb smaller companies efficiently. If this isn’t done, add-ons can easily turn from assets into liabilities.

Process Flow 1: Buy-and-Build Strategy — End-to-End Execution

| Phase | Key Activity | Typical Duration | Primary Owner |

| 1. Strategy Design | Create a target sector, platform requirements, and add-on profile | 1–3 months pre-close | Investment Team |

| 2. Platform Acquisition | Look for sources, diligence, and obtain an anchor company. | 6–12 months | Deal Team / Advisors |

| 3. Foundation Setting | Set up management and reporting systems, integration playbook | 0–6 months post-close | Operating Partners |

| 4. Add-On Sourcing | Recognize, approach and assess acquisition opportunities | Ongoing (years 1–4) | Handle Team + Platform Mgmt |

| 5. Add-On Execution | Close individual add-ons by negotiating, structuring and closing. | 2–6 months per deal | Legal / Finance / Deal Team |

| 6. Integration | Integrate operations, systems, culture and reporting | 3–12 months per add-on | Operating Partners + Mgmt |

| 7. Value Harvesting | Optimize the group and prepare the exit narrative, market to buyers | 12–24 months pre-exit | Investment Team + Advisors |

| 8. Exit | Go to a strategic buyer, secondary PE, or go public | 6–12 months | Investment Team / Bankers |

The Five Steps to Executing a Successful Add-On Acquisition

In any transaction, there are varying aspects to consider, but there is a common methodology that is followed in the execution of an add-on acquisition in a buy-and-build private equity transaction. This process can be summarized in five steps below that can be used by professionals of all experience levels.

Step 1 — Define the Add-On Criteria Before You Begin Sourcing

The biggest pitfall of add-on sourcing is searching before developing an acquisition thesis. The investment team and platform management need to agree on the characteristics of the ideal add-on to target before they approach any target: its geographic spread, revenue level, customer concentrations, minimum margins on EBITDA, and cultural compatibility. At this stage, precision is a huge timesaver and helps the organization avoid looking into deals that seem good at first glance but won’t proceed with the strategic thesis.

Step 2 — Build a Proprietary Deal Pipeline

Broadly marketed processes are key for the most value-accretive add-on acquisitions. Rather, they arise over time, directly from business owners, through introductions by industry contacts, or through a gradual and systematic approach in reaching out to prospective business owners that may not have decided to sell. A platform management team is another source of deal ideas that many don’t use and they generally know their competing landscape very well. It’s a long and steady process to build a proprietary pipeline, but it consistently provides the best pricing and deal terms as compared to competitive auctions.

Step 3 — Apply Disciplined Deal Structuring Valuation Techniques

Valuation of the add-on acquisitions must be done with proper application of deal structuring valuation techniques, taking into consideration the standalone value as well as synergy potential. One way of doing this is to value the target on its standalone merits first (using comparable transaction multiples, discounted cash flow analysis and earnings normalization) and then separately considering the synergy case, with a view to how much (if any) of the synergy value is to be allocated to the seller in the purchase price. It helps avoid overpaying on synergies, which are not always realized, and has been a problem for many buy-and-build programs.

Step 4 — Structure the Deal to Align Incentives

Add-on acquisitions often are comprised of sellers who will stay with the business after the sale or purchase — either as a minority shareholder or as a manager. It’s important to structure the transaction in a way that makes their incentives work for the success of your platform. This frequently includes earn-out provisions based on future outcomes of financial statements, rollover equity, retention of key individuals, and other provisions. Nailing down the structuring and valuation of the deals will take some work, and it’s important to have a reality check on each seller’s motivations.

Step 5 — Execute Integration with the Same Rigor as the Deal Itself

Buy and build value is realized or destroyed in the process of integration. Applying a 100-day integration plan suitable for people, systems, processes and culture provides the best opportunity for the integrated business to achieve planned synergies without sacrificing the momentum of the acquired business’s operations. The most sophisticated practitioners keep integration milestones as closely monitored as financial covenants and view integration management as a key and value-enhancing capability, not an add-on to the deal.

Table 1: Add-On Acquisition Valuation Framework — Key Inputs

| Valuation Element | What It Measures | Typical Approach |

| Standalone EBITDA | Earnings before non-recurring and platform costs. | Normalization of owner salary, one-off costs, and related-party items |

| Entry Multiple | Price paid as a multiple of normalized EBITDA | Comparable transactions; negotiation anchored by strategic fit |

| Synergy Estimate | Savings in revenue and costs after integration | Bottom-up analysis; haircut applied for execution risk |

| Earn-Out Component | Reward based on achievement of targets | A range of 12–36 months and subject to EBITDA and/or revenue milestones. |

| Rollover Equity | Seller’s reinvestment in the larger platform. | Typically 10–30% of deal proceeds; aligns long-term incentives |

| Pro-Forma Combined EBITDA | Earnings from platform + add-ons with synergies applied | Used to assess the impact on group leverage and exit valuation |

Real-World Examples and Lessons from the Field

The veterinary services industry is a textbook example of the buy and build private equity strategy and its opportunities and challenges. In the ten years that have passed, there have been a series of private equity firms from Europe that have gone on an aggressive buying spree of independent veterinary practices. The Spicer case, which was well documented, was a mid-market fund from London that bought a regional veterinary group as the platform and made nineteen add-on investments in five years. At exit, there were forty-two clinics and the revenue had grown more than 400 percent. The exit multiple (via a global strategic sale) was almost double the entry multiple, and the return on invested capital was more than three times.

The key to success in this program was three things that the investment team identified and they did not waver on. First, it was platform management that was outstanding – the founder veterinarian had established a good network in the veterinary industry and could approach independent clinic owners as equals and not as a financial buyer. Second, early on, integration was a relatively light touch: clinics were kept separate, under the same brand, the same personnel, and the same local name, but shared the administrative structure, procurement and clinical processes. Third, consistent deal structuring valuation techniques were used – the team kept its pricing discipline as it walked away from a desirable acquisition if the price was not attractive and revisited the target at a later stage.

An example of this would be the dental sector in North America, where a private equity-backed group of businesses went on an aggressive add-on program without having the appropriate infrastructure in place to integrate it. In less than three years, the platform closed fourteen acquisitions, more than the management team and IT infrastructure could handle. Quality control problems surfaced at various locations, staff turnover grew as the traditional culture of individual practices was undermined, and a number of earn-out sellers have turned hostile if performance objectives were not met, in part because of the disruption of the integration process. In the end, the company needed a big restructuring in its operations before it would be sold and the result was far below the expectations in the original investment case. The lesson was as hard as it was to accept: the speed of acquisition needs to match the capacity for integration, and the process of value creation that private equity relies on – on people and on process – must be as much investment as on financial engineering.

Process Flow 2: Add-On Acquisition — From Identification to Integration Close

| Step | Activity | Key Stakeholders | Watch Point |

| 1 | Target identification via proprietary outreach or intermediary | Deal Team, Platform CEO | Avoid competitive auctions where possible |

| 2 | Preliminary meeting & NDA execution | Deal Team, Target Owner | Assess cultural fit early — do not leave it to diligence |

| 3 | Indicative offer / Letter of Intent | Deal Team, CFO | Anchor pricing on normalised EBITDA, not headline revenue |

| 4 | Financial, legal & operational due diligence | Advisors, Compliance, Ops | Scrutinise customer concentration and key-man dependency |

| 5 | SPA negotiation & structuring | Legal, Deal Team, Finance | Balance earn-out incentives against complexity and disputes |

| 6 | Regulatory / competition clearance (if applicable) | Legal, Compliance | Allow adequate timeline; do not assume clearance is automatic |

| 7 | Close & Day 1 readiness | Platform CEO, HR, Finance | Communicate clearly to all employees on Day 1 |

| 8 | 100-day integration plan execution | Operating Partners, Mgmt | Track milestones weekly; escalate blockers immediately |

| 9 | Integration close & performance review | Investment Team, Platform | Capture lessons learned for next add-on |

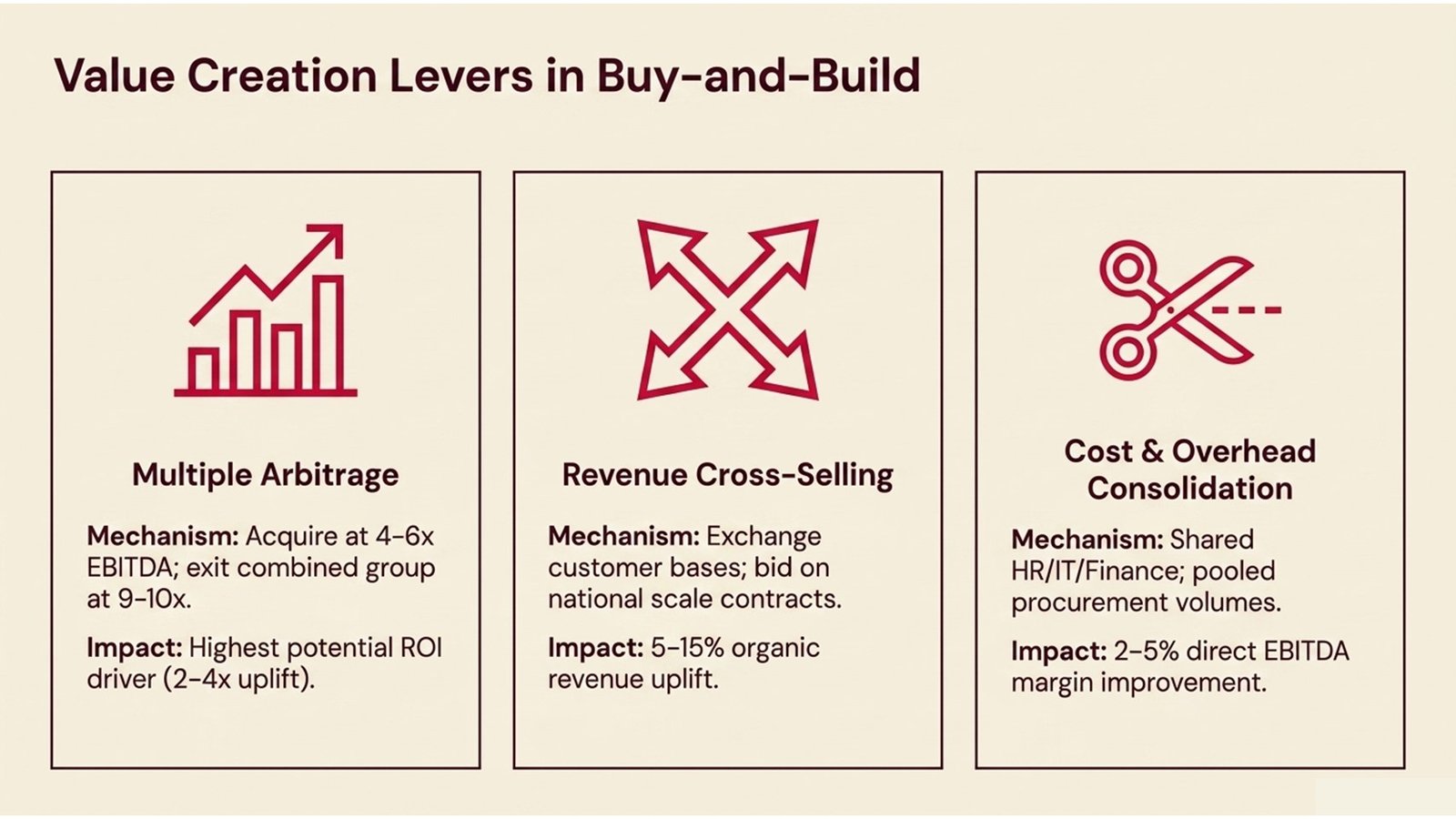

Value Creation Levers and How They Work Together

The private equity value creation strategies utilized in a buy-and-build program play out on a variety of interrelated fronts. The most apparent lever is multiple expansion, with the caveat that this is backed by operational improvements and revenues that allow the buyer at exit to pay a premium. It is important for professionals to understand how these levers affect each other in order to participate in or assess a buy-and-build program.

Cross-selling — marketing products and services from one acquired company to customers of another — and geographic scale and brand recognition, can all help to drive growth in a consolidated platform. A ‘group’ of regional maintenance and inspection companies, for example, may tender for national contracts for large corporate clients which would not have been viable for any single company. This capability in securing bulkier contracts in turn alters the quality of the revenue base and the potential of exit multiple.

Cost efficiencies generated through consolidation represent another core private equity value creation strategy lever. Combined purchasing volumes, sharing back-office functions like finance, HR and IT, and eliminating duplicated overhead with acquired businesses are all factors in procurement savings, which helps expand margins. However, it is important to note that these synergies are not always found by chance; they must be managed and nurtured, systems need to be invested in, and, sometimes, difficult decisions need to be made on organizational structures. The most rigorous practitioners show synergy in detail when they make each acquisition and monitor the realization of synergy with the same detailed precision as they would do in financial reporting. This is also one of the most important disciplines in deal structuring that should be considered at entry: only synergy that can be achieved is included in purchase price assumptions.

Table 2: Key Value Creation Levers in a Buy-and-Build Program

| Value Creation Lever | Mechanism | Typical Impact | Risk if Poorly Managed |

| Multiple Arbitrage | Acquire small add-ons at lower multiples than the platform’s exit multiple | High — can drive 2–4x uplift | Overpaying for add-ons erodes the arbitrage benefit |

| Revenue Cross-Selling | Sell platform services to add-on customer base and vice versa | Medium — 5–15% revenue uplift | Cultural resistance; customer disruption if rushed |

| Procurement Savings | Aggregate purchasing volumes across all entities | Medium — 2–5% EBITDA margin improvement | Requires a centralized procurement function |

| Overhead Consolidation | Share finance, HR, IT, and administration across the group | Medium-High — removes duplicated cost | Staff morale issues, if managed poorly |

| Management Professionalisation | Replace founder-led informality with scalable leadership | High at exit — improves acquirer confidence | Key-man risk during the transition period |

| Organic Growth Reinvestment | Redirect savings into growth initiatives | Variable — depends on sector dynamics | Undermines synergy targets if not ring-fenced |

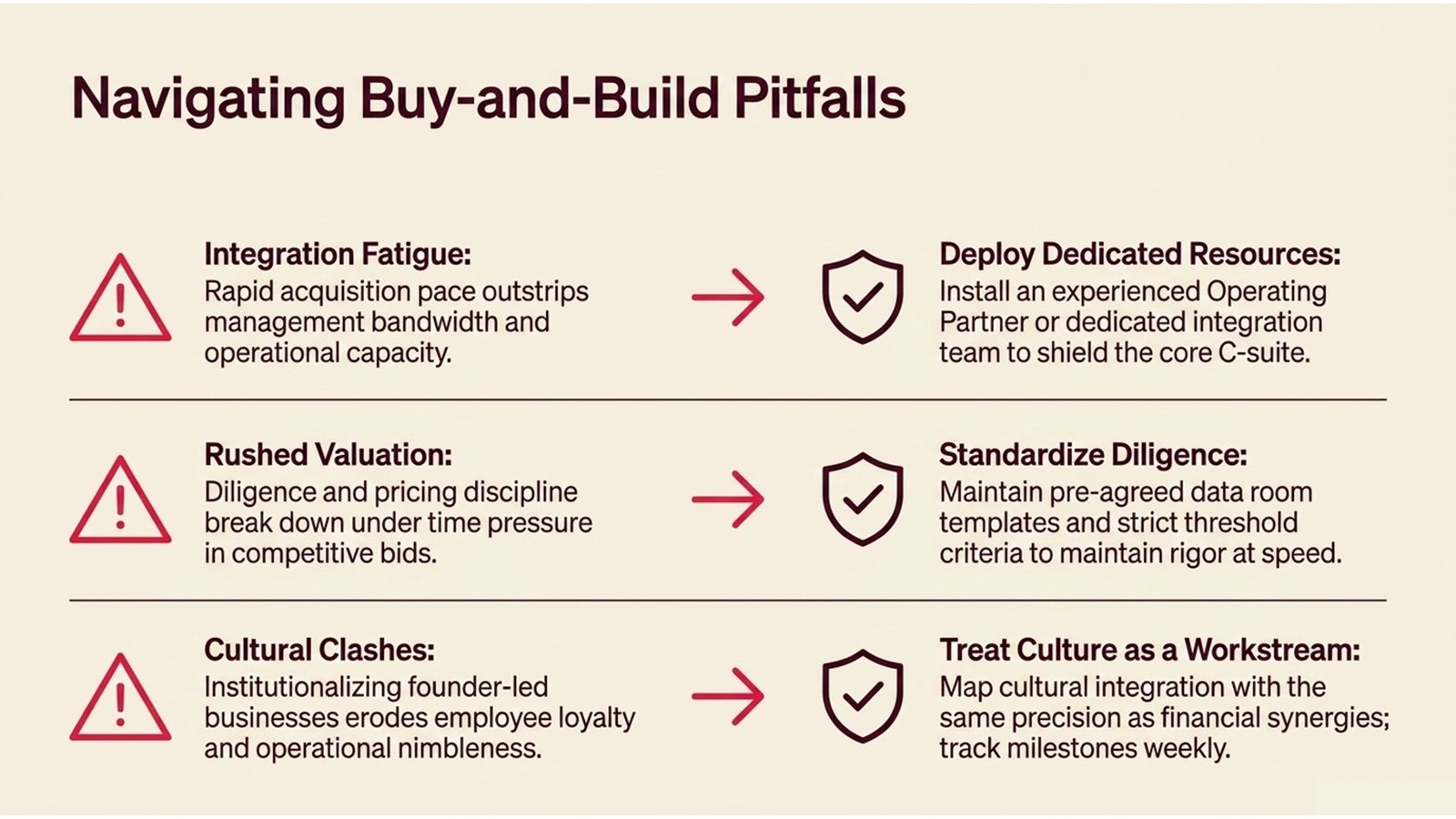

Challenges, Common Pitfalls, and How to Navigate Them

The buy-and-build private equity strategy, although popular, is one of the most operationally complicated strategies of private equity. The challenges are authentic, frequent, and, a key factor for any professional developing their career, educational. It’s as important to know where and why these strategies fail as it is to know where and why they are effective.

The challenge of integration fatigue is one that has been present for a long time. As a platform performs a number of add-on applications concurrently, or sequentially in quick succession, the management team gets spread across a growing portfolio of integration projects. Operating current companies takes a lot of attention and it is competing with the attention that is needed to absorb another company on a daily basis. Companies that have been able to overcome this hurdle generally do so by investing in integration resources that contain an operating partner with experience in the process or a small team of internal integrators whose job is to execute the post-close process without taking up any bandwidth from the platform’s senior leadership.

Another difficulty is with the accuracy of deal structuring valuation techniques in a hurry. Competitive add-on situations can tend to rush deal teams to rush through the deal process and price with less information. This is where practicing discipline in the process is the most important. Well-experienced practitioners usually have a standing template of the data room—an agreed checklist of the financial, legal, operational and commercial information that must be provided prior to any price call—ready to go and deploy quickly without compromising on quality. Those companies that adhere to it make better acquisitions than those whose speed is at the expense of rigor.

A third challenge is the one of cultural integration, which is often underestimated and under-resourced. Buy and build add-on targets, which generally constitute the bulk of the businesses, are often run in a highly personal manner, with a culture established by the founding owner. Acquired and merged into a larger and more institutionalized platform, culture clashes can undermine the operational nimbleness, customer intimacy, employee loyalty, and other factors that make the acquisition appealing. What really works in the long run is the private equity value creation strategies that make the cultural integration a clear workstream, have specific staff resources assigned, have specific milestones and conduct regular pulse checking on employee engagement across the group.

Conclusion: Actionable Insights for Finance Professionals

Buy and build is one of the most compelling models — and most challenging — of private equity. If done properly, it provides returns that are much higher than those resulting from standalone acquisitions and produces businesses of scale and sustainability. If not done properly, it results in expensive integration problems and less successful exits that tie up management time for years. The disparity between these results is not usually because the deals are bad or good, it’s almost always because the execution of them is bad or good.

Several spanners are thrown into the works from the frameworks and examples discussed in this article for those professionals who are developing a career in private equity, M&A advisory, or corporate finance. First, go to a conceptual level and get a real grasp of the buy and build strategy in private equity, not only the financial aspects, but the business rationale behind it, too. The ability to clearly explain why an industry is ripe for consolidation, the importance of a strong versus a not-so-strong “platform”, and how the criteria of adding value on a “platform” should be structured relative to a specific thesis will make you shine in interviews, deal teams, and advisory meetings.

Second, build real-world expertise in the valuation methods that are used in the structuring of deals in an add-on transaction. This involves more than just the textbook DCF and similar company analysis, but understanding how practitioners normalize earnings, value synergies, design earn-outs, and structure rollover equity. This is sophisticated, and the more comfortable practitioners who can seamlessly navigate between financial modeling, legal negotiation, and commercial assessment are always the most sought-after team members on any deal team.

Next, take care of the integration. No, it’s easy to just concentrate on the deal and let someone else handle the integration—especially at the beginning of a career. However, the most business-savvy professionals know that integration is the key to the success of private equity value creation strategies or failure. Proposing to support 100-day plans, monitoring synergy delivery, and overseeing the day-to-day management of a post-close transition will provide exposure to the elements of a deal cycle that directly relate to return outcomes.

Fourth, study real examples — including failures. The dental services case mentioned above is only one of a number of previously-reported examples of buy-and-build programs that got out of hand. Knowing the nuances of each decision, and thus the outcomes, will make you a better analyst and more believable advisor. The private equity world has a lot of institutional knowledge and those who are interested in learning from others’ experiences make significant strides in their learning.

Last, but not least, have a long-term mindset for the buy-and-build private equity strategy. These are long-term programs that take time, consistency and discipline to pursue, and be prepared to reject acquisitions that don’t align with the criteria, even if there is pressure on deals and the pipeline is thin. The ones who are successful in this environment are the ones who have analytical rigor and sound judgment, and are aware that the highest returns of private equity are not from a single great deal, but from a consistent focus on disciplined private equity value creation strategies over the course of the entire investment cycle.