Portfolio Turnaround in Private Equity

Not all private equity acquisitions are as planned. Market environments change, managerial capabilities fail to perform as well as expected, cost bases are less adaptable than expected, and market competition changes more quickly than the initial investment thesis supposition. The question of what actions the private equity firm can take to help a portfolio company, and when, how, and to what extent, is one of the most significant choices they will face once the portfolio company starts to perform poorly. One of the most challenging areas in deal-based finance is the use of private equity turnaround strategies, which require a combination of strategic acuity, operational acumen, financial engineering, and decisive leadership.

The antecedents are great on either side of the equation. A successful turnaround will transform a struggling asset into an interesting exit story and yield returns that justify the initial acquisition thesis, even when initial assumptions were incorrect. An intervention that is mismanaged, in turn, may hasten a firm’s decline, erode trust among stakeholders, and cause a write-down that takes a toll on the fund’s overall performance. Knowing how the turnaround process works is thus not only vital to those employed within a PE firm but also to those in investment banking, restructuring advisory, strategy consulting, and corporate development who deal with PE-backed businesses at pivotal moments.

This paper provides a pragmatic summary of private equity portfolio management in distressed or underperforming scenarios. It addresses the diagnostic process, the five key steps of execution, real-life examples, likely issues to be encountered, and M&A as a turnaround accelerator. In the process, it taps into values instilled in hardcore mergers and acquisitions training, which treats deal execution and post-acquisition value creation as indivisible.

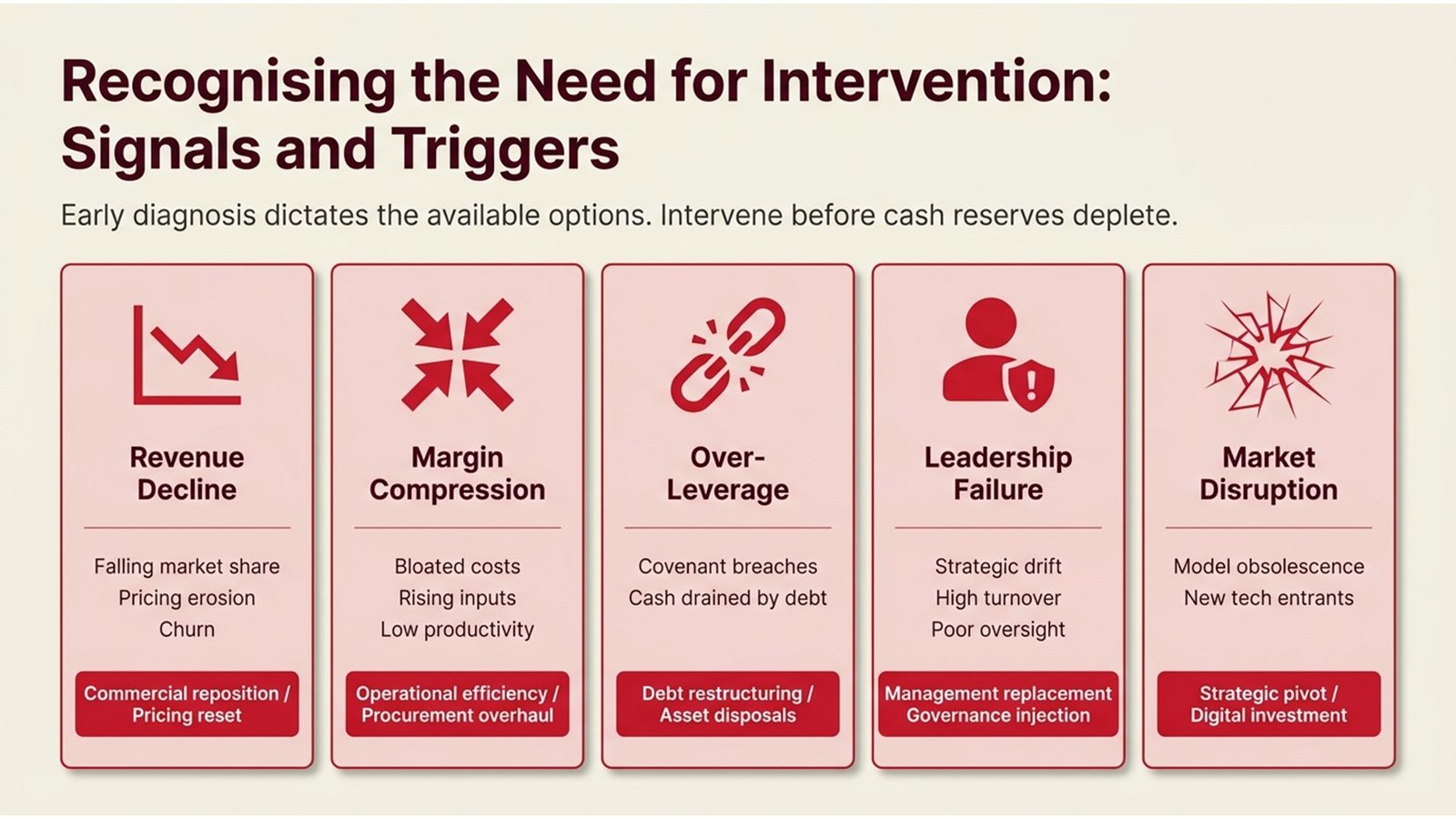

Recognizing the Need for Intervention: Signals and Triggers

The initial difficulty in any turnaround situation is time. PE firms that act too late when they run out of cash, when management credibility is lost, or the lenders have lost faith have a much more limited range of choices than those that can identify the signs of stress and take decisive action. The early warning system that signals deterioration prior to a crisis is a well-organized management system for a private equity portfolio that includes quarterly performance reviews, monthly cash flow reviews, and board participation.

The causes of a formal turnaround program are quite diverse and differ in extent. The loss of market share, product or service price erosion, a threat of customer concentration, or a product line losing relevance demands a different response to cost-side distress, where input inflation, operational inefficiency, or an excessive overhead base is squeezing margins. Structural balance sheet issues, such as covenant violations, refinancing risk, or debt service consuming an unsustainable amount of free cash flow, add a third dimension that limits available options and usually necessitates both operational and financial restructuring.

Among the most underestimated turnaround triggers are governance and leadership failures. Even the best-designed operational strategy can be counteracted by a management team that is incompetent, inexperienced, or even non-urgent to implement a transformation plan. PE firms whose networks with operating partners enable them to have a deep understanding of the industry are well placed to detect leadership lapses early on and take decisive action. One of the most crucial diagnostic skills in the turnaround toolkit is the ability to distinguish a leadership problem and a structural business problem – or more likely their combination. The most common turnaround triggers and the PE responses summarised are presented in Table 1 below.

Table 1: Common PE Turnaround Triggers and Responses

| Turnaround Trigger | Typical Symptoms | Primary PE Response |

| Revenue Decline | Loss of market share, price deterioration, loss of customers. | Rebranding and resetting of the pricing strategy. |

| Margin Compression | Increasing input costs, a swollen cost base, and poor productivity. | Program for operational efficiency and procurement overhaul. |

| Over-Leverage | Cash-flow-depleting debt service; covenant violations. | Restructuring of debt, capital infusion, and selling off of assets. |

| Leadership Failure | This is due to strategic drift, excessive executive turnover, and inadequate board supervision. | Replacement of management, strengthening of the governance. |

| Market Disruption | Entrants in the business model, new technology. | Pivot, bolts, and online investment. |

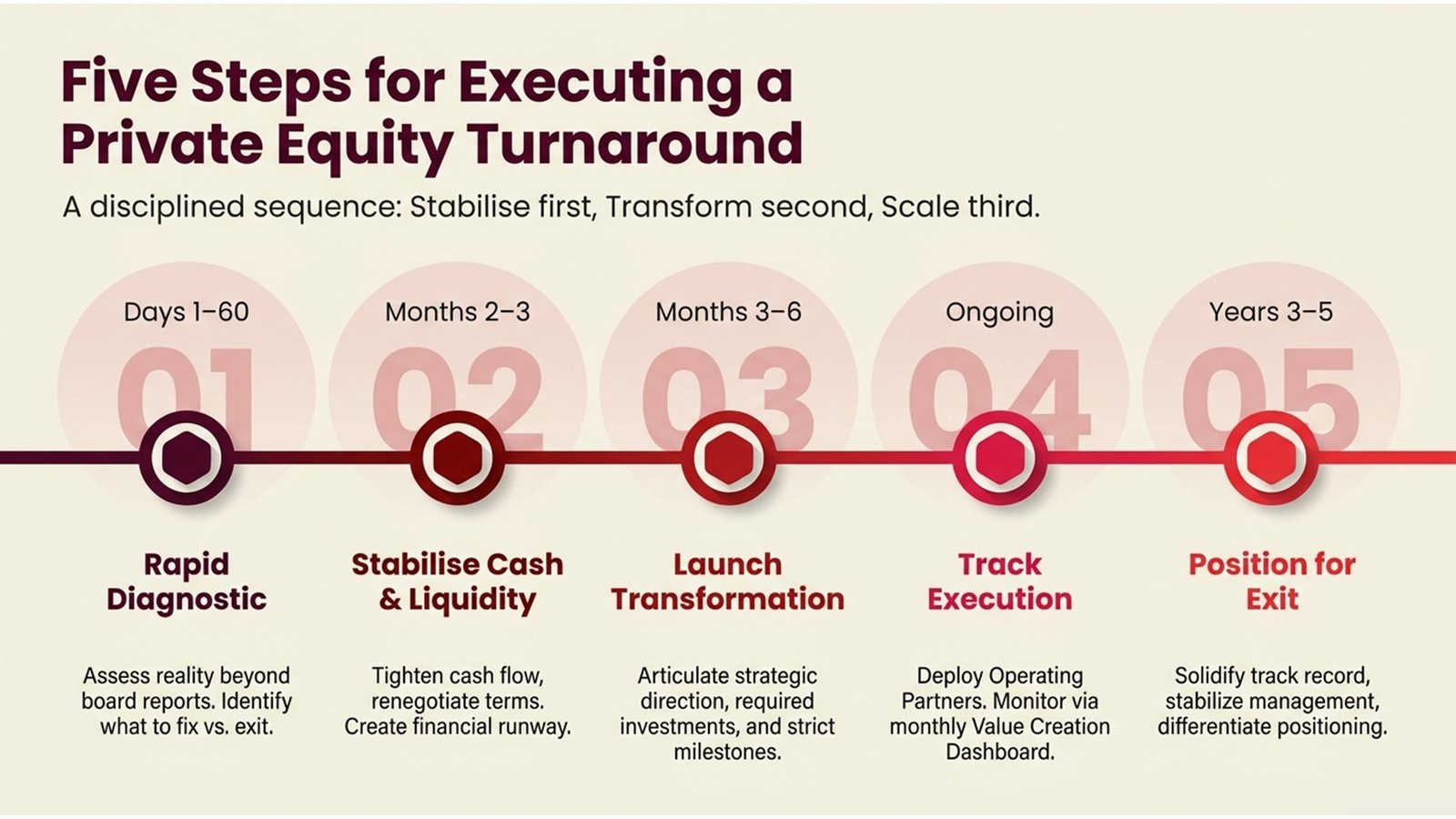

Five Steps for Executing a Private Equity Turnaround

Good private equity turnaround programs have a rigorous process with defined steps. The exact content of each step will depend on the circumstances, but the logic of stabilization, transformation, and scale remains the same across industries and regions. The five steps below reflect best practices based on practitioner experience, as well as formal mergers and acquisitions training that is as strict in addressing post-deal value creation as it is in pre-deal assessment.

Process Flow 1: The 5-Step PE Turnaround Execution Framework

| Step 1 | Step 2 | Step 3 | Step 4 | Step 5 |

| Rapid Diagnostic (Days 1-60) | Stabilize Cash & Liquidity (Month 2-3) | Design & Launch Transformation Plan (Month 3-6) | Implement & monitor through Value Creation Dashboard (Continuous) | Position For Exit (Year 3-5) |

Step 1 — Rapid Diagnostic. The information-rich part of the whole process is the first sixty days following a turnaround. The PE firm and its advisers need to rapidly develop a clear vision of the business’s financial situation, business realities, and competitive landscape. It is much more than the examination of management accounts; it is about talking to customers, suppliers, and front-line employees whose opinions are seldom seen in board-level reporting. The diagnostic phase is supposed to give a clear evaluation of what is structurally sound, what is fixable, and what is to be bailed out.

Step 2 — Stabilize Cash and Liquidity. Any business should be financially stable enough to implement any transformation program before it can take off. This will normally involve rigorous cash flow control, renegotiating payment terms with major suppliers, speeding up debtors’ collection, and, when needed, negotiating with lenders for a covenant waiver or temporary refinancing. The aim is to have a long runway for financial changes to start yielding results. This phase is characterized by challenging negotiations with lenders and creditors, and, most of the time, the services of restructuring experts are required.

Step 3 — Design and Launch the Transformation Plan. Once the business is stabilized, the private equity firm and the management team can develop a viable medium-term transformation plan. This report must spell out the new strategic path, the targeted operational projects to drive improvement, the funding required, the personnel responsible for implementing them, and the milestones to measure improvement. Too vague plans are more aspirational than specific; they can hardly build the management commitment and investor trust needed to undertake a successful turnaround.

Step 4 — Execute and Track via a Value Creation Dashboard. Most turnaround plans succeed or fail at implementation. The operating partners of the PE firm are usually actively involved at this stage and work in conjunction with management on workstreams, rather than serving on the board and watching over management’s shoulder. The transparency provided by a monthly value-creation dashboard that monitors key leading and lagging indicators aligned with the transformation plan will help identify gaps promptly and ensure they do not compound. Good, disciplined management of the private equity portfolio in operational reporting is a hallmark of the most successful PE firms.

Step 5 — Position for Exit. This will mean having a strong financial record for the business that will help tell a compelling investment story, a credible and stable management team, and clear, differentiated strategic positioning. Regardless of the planned exit path, whether a trade sale, secondary buyout, or IPO, it is recommended that preparations be made at least a year and a half prior to the intended transaction. Mergers and acquisitions advisers and bankers who have been around training have always stressed that the exit preparation is a process, rather than an event.

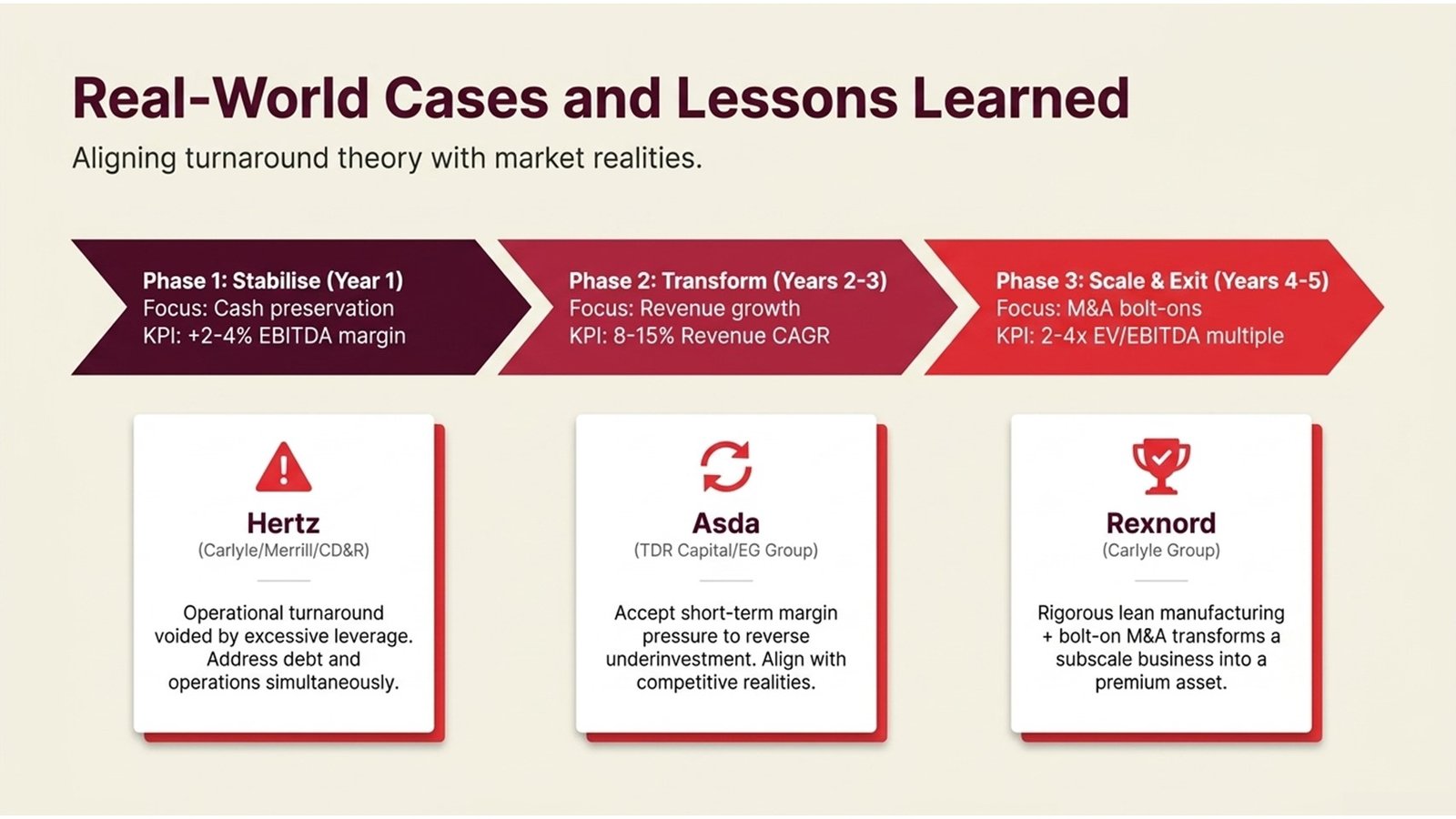

Real-World Cases and Lessons Learned

Both the strengths and the weaknesses of PE-led transformation can be exemplified by the turnaround of Hertz by Clayton, Dubilier & Rice, Carlyle Group, and Merrill Lynch Private Equity, which occurred after Ford Motor Company in 2005. The consortium initially realized significant value in cost reduction and fleet optimization, but the business had substantial debt, which exposed it to the 2008-09 financial crisis. A warning that business structural balance sheet risk does not necessarily protect a business when operational turnarounds are implemented, Hertz declared bankruptcy in 2020. The lesson for practitioners is that private equity turnaround strategies must address leverage and operational performance simultaneously, not sequentially.

An even more educational example is the turnaround of Asda’s assets by TDR Capital and EG Group, which bought the UK supermarket from Walmart in 2021. With a business that had lost significant market share to discounters Aldi and Lidl, and with a large property and cost base, the new owners embarked on a vigorous store investment program, price repositioning, and supply chain restructuring. The plan recognized that, to turn years of underinvestment around, it was necessary to take a short-term margin in exchange for a long-term, credible, competitive position. Although the turnaround continues to unfold, the case underscores the need to align the transformation strategy with market realities rather than merely optimizing near-term EBITDA.

The Carlyle Group’s turnaround of Rexnord provides a textbook example of how value can be unlocked in a multi-site manufacturing company through a disciplined portfolio-management approach by a private equity firm investing in complex industries. In 2002, Carlyle bought Rexnord, which had overly high legacy costs and an unconcentrated product line. The company followed a hard-and-fast lean manufacturing program, rationalized the product range, divested non-core lines of business, and made selective bolt-on acquisitions to strengthen its position in high-margin niche markets over the next few years. By the time it was finally publicly listed, Rexnord had been turned into a small-scale industrial conglomerate and had become a niche, high-quality engineering company with a high market multiple.

Table 2: Value Creation Levers by Holding Phase

| Holding Phase | Priority Lever | Typical KPI Target |

| Year 1 (Stabilize) | Conservation of cash, fast payback, and cost-cutting. | 2-4 ppt improvement of EBITDA margin. |

| Years 2-3 (Transform) | Increase in revenue, restructuring of operations, and a capex reset. | Revenue CAGR of 8-15% |

| Years 4-5 (Scale & Exit) | Bolt-ons of M&A, market expansion, and exit preparation. | 2-4x EV/ EBITDA multiple growth. |

Processes, Challenges, and the Role of M&A in Turnarounds

The operational transformation and financial stability demands can coexist and are among the most complex aspects of implementing private equity turnaround strategies. The temptation to postpone some tough operations, such as reorganizing a workforce, shutting down non-performing business units, and renegotiating customer contracts, because of the pain and suffering they cause in the short run, is quite natural but always counterproductive. Turnarounds that place greater emphasis on financial engineering than on actual operational change are likely to yield unsound results that collapse in the face of the next market crash.

M&A, especially bolt-on acquisitions, is taking a greater role in PE turnaround. A poorly performing portfolio company that is not large, has limited geographic or product coverage, or both, may discover that organic enhancement is insufficient to achieve the competitive repositioning needed. A well-selected acquisition can accelerate revenue growth, reduce an unwanted cost base, and provide the business with management talent or technological resources it already lacks. This is why individuals with strong mergers and acquisitions training (who are not only aware of how to evaluate and execute transactions but also how to integrate post-merger) are very useful, especially in PE-backed turnaround cases. Any bolt-on acquisition, particularly when it is also a business-facing transformation, requires a thought sequence to prevent overloading management bandwidth.

One of the most constantly under-evaluated issues in PE turnarounds is people management. A change in a CEO or CFO creates uncertainty, which may affect morale, customer relations, and lenders’ confidence. The sensitivity and specificity required to retain key talent in operations while providing the leadership changes needed to implement change are not always easy for deal-oriented professionals to attain. The most proficient PE practitioners in the turnaround arena have learned to distinguish between leaders who are genuinely unable to effect the necessary change and those who, with clearer direction, proper incentives, and support, can stand up to the task.

Process Flow 2: M&A Bolt-On Process within a PE Turnaround

| Phase 1 | Phase 2 | Phase 3 | Phase 4 | Phase 5 | Phase 6 |

| Strategic Reasoning & Target Visitation. | Preliminary Diligence & LOI | Complete Due Diligence (Financial, Legal, Commercial) | Valuation & Deal Structuring | SPA Negotiation & Close | Integration Planning & 100-Day Implementation. |

Another challenge that is usually handled reactively, rather than proactively, is stakeholder communication. The employees, customers, suppliers, and lenders are directly interested in the progress of the turnaround, and their ongoing faith is usually necessary for it. A business that loses its critical customers due to uncertainty about its future, or loses its skilled employees due to rumors of restructuring makes its recovery more difficult. Creating a clear, consistent, and credible communication plan, one that is truthful about the difficulties yet shows an understanding of the way forward, is an element of turnaround implementation that should be given similar focus as the financial model.

Building Skills for Turnaround and Portfolio Work

The PE turnaround experience is one of the most challenging and rewarding learning curves in corporate finance for junior- and mid-level financial professionals. The scope of skills needed, which includes financial analysis, operations evaluation, strategic thinking, and negotiation, as well as stakeholder management, is hardly paralleled in other settings. Gaining an insight into the practice rather than the theory of managing a portfolio in the context of a private equity firm provides a base that can be useful in investment banking, private equity, consulting, and corporate functions.

Mergers and acquisitions training that is structured and integrates post-deal value creation and portfolio management (rather than selling the deal at deal close) is also especially useful for professionals who desire a more holistic view of the PE process. Numerous training courses focus on deal origination, valuation, and deal structuring, which are undoubtedly crucial skills. Still, the most rapidly progressing professionals in PE-oriented careers are those able to convincingly present themselves to the operational and strategic issues that emerge once an operation has been made, such as the stressful dynamics of a turnaround scenario.

In practice, practitioners in lower levels of the career ladder can develop the requisite skills through learning documented turnaround cases in detail, not just what strategies were used, but how decisions were made amidst uncertainty, how stakeholders were handled, and what was special about the interventions that worked and those that did not. After the experiences of working with partners in large PE firms, reading restructuring advisory books, and finding positions that allow one to have a real experience of the operations of portfolio companies as opposed to transaction work, are all avenues to building that competency that private equity turnaround strategies require. The experts who excel in this field are among the most in demand.

Conclusion: Actionable Insights for Finance Professionals

One of the most complex and impactful issues in deal-driven finance is the turnaround of private equity portfolios. They require intellectual integrity regarding what has gone awry, operational integrity in developing and implementing a recovery plan, financial acumen in handling the balance sheet during the transformation, and human judgment in dealing with the people aspects that so frequently make or break a strategy.

To attain expertise in the field, a number of practical measures can be highlighted for professionals who wish to develop it. First, get a good foundation in the principles of financial restructuring – learn the mechanics of covenants, how a situation of distress arises, and what can be done at various levels of stress on the balance sheet. Second, invest in training for mergers and acquisitions that focuses on post-deal integration and portfolio management, and on deal execution skills that have been most likely to be taught in the curriculum. Valuable programs consider value creation a discipline that encompasses the full cycle, rather than one that comes after the deal has been signed.

Third, examine the actual cases of turnaround. The examples of Rexnord, Asda, and Hertz presented in this article all offer valuable lessons in strategy, implementation, time, and risk management that are well worth studying. Fourth, find ways to work with businesses undergoing operational change, be it through advisory services, operating partner attachments, or corporate development activities within PE-backed companies, since the experiential learning available in such settings is not easily replicated in other settings. Lastly, learn how to communicate and manage stakeholders, which technical finance training seldom focuses on, but which practitioners repeatedly mention as one of the determining factors of turnaround success.

Financial engineering in isolation is not the best way to manage a private equity portfolio. It has to do with the establishment of real, sustainable business value in challenging circumstances – and those professionals who can perceive that difference, and can practice it, will find that specialization in turnaround in the private equity business is one of the most intellectually interesting and professionally gratifying fields of finance.