Introduction to Comparison of PE VC and IB Fund Structure for Beginners

In financial circles, the structure of an investment vehicle has far reaching implications on the capital raising, deployment, management, and capital returned to investors. Such industries as Private Equity (PE), Venture Capital (VC), and Investment Banking (IB) are among the most famous participants of the financial eco-system which have their specific structure, operational model, and strategic goals. Although the three sectors have a similar aim that is to help channel capital to make returns, their operations are governed by various structures that affect risk appetite, investment periods, governance and the value creation strategies. The differentiation of the fund structure is crucial knowledge to any investor, fund managers, corporate management and anyone dealing in the capital market.

These distinctions cannot be described as academic only, as they define the experience of an investor, the kind of projects they are willing to fund, an industry they want to address, and how involved in the operation they want to get. This discussion will revolve around the primary structure of each of the models, the lifecycle of investments, the source of capital and process by which each model stands out among the other.

Briefly analyzing the elements of its structure we can better understand how each of them uniquely contributes to the sphere of global finance and why this or that project should be implemented within one or another type of fund. For professionals seeking practical applications, enrolling in an Industry-specific PE/VC course in Singapore can provide the skills and insights needed to navigate these complex structures effectively.

Private Equity Fund Structure and Operational Model

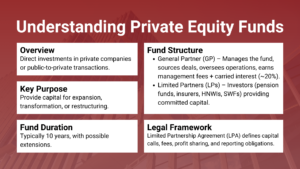

The Private Equity funds are normally structured as a limited partnership where the fund manager or general partner (GP) and the actual investors (limited partners LP) are limited partners who own the fund. The role of the GP specifically is to raise capital, find investment opportunities, do due diligence and manage as well as exit the investment. Typically the institutional investors, who invest in the LPs, are pension funds, insurance companies, sovereign wealth funds, and high-net-worth individuals, who can commit capital to an LP on a fixed-term basis-typically ten years-under the agreement that they can take out the money as needed, instead of holding it as a lump sum.

The fixation with control and active operations is one of the features of PE fund structure. PE funds can take control of a company (where allowed by corporate law) as opposed to some types of investment vehicles which can only leverage their interest by financial engineering alone. The closed-end character of the fund implies that capital is used during a certain time before being distributed to investors when the portfolio companies are sold, merged with, or offered publicly to investors.

PE fees are usually in the form of a management fee which is usually around two percent of committed capital, and a performance fee or a carried interest which is commonly two percent of the profit beyond a prescribed hurdle rate. This is because it aligns the incentives between GPs and LPs and keeps the fund managers interested in making as much money as possible throughout the existence of the fund. It, however, puts considerable pressure on GPs to effectively choose investments that match risk/reward alongside good governance and effective operations.

Venture Capital Fund Structure and Investment Approach

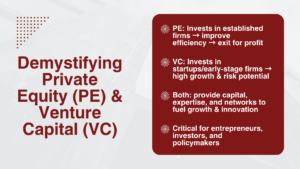

Venture Capital is structurally similar to Private Equity since most of them are usually set as limited partnerships involving GPs and LPs. Nevertheless, the approach towards operation, risk profile and investment thesis are very different. VC funding is directed mostly at younger and high-growth potential businesses, typically within technology, biotechnology and the more innovative industries. Such investments are likely to be in minority equity positions not gaining control; they are more focused on increasing growth rate than reorganization of operations.

The nature of ventures at the early stages has to be taken into consideration in the structure of the funds a VC invests. Although PE deals usually display a more evident way to profitability upside, VC-funded startup companies may not attain a positive cashflow for years, but have to grow with successive cash injections. This implies that portfolios of VC funds are relying on a small number of outstanding investments referred to as home runs to give returns on most of the companies that underperform or fail.

Capital commitment period VC funds like PE have a typical period of ten years with the first few years spent in active sourcing and funding of startups and then a few years of governance of such investments followed by either exiting via IPOs or through acquisitions. The profile of returns is more volatile, but there can be large potential performance as the fund acquires equity in a company that becomes a market leader or disrupts an industry.

Regarding the fee structure VC funds also perform under the two and twenty model but their performance largely relies on the capacity to detect opportunities in emerging markets, establishment of connections with entrepreneurs and co-investors and ability to provide strategic advice to the founders without necessarily assuming direct control of the business. For those looking to build expertise in this field, a Venture capital course for professionals provides structured knowledge and practical frameworks to understand these dynamics.

Investment Banking Structures and Revenue Models

Investment Banking does not take a closed-end investment form, as compared to PE and VC. Rather, the investment banks are corporate institutions that supply their services on the basis of advisory, underwriting, and capital raising options to their customers such as businesses, governmental bodies and also to the case of institutional investors. It is a service-based (as opposed to fund-based) structure which means that investment banks derive income in the form of transaction fees, advisory retainers, underwriting spreads and trading commissions as opposed to the long-term returns of equity.

The investment banks are structured in terms of various divisions with each playing a unique role in the capital markets. Merger and acquisition, restructuring and capital raising are done by the corporate finance or advisory branch. The sales and trading unit helps institutional clients to trade in the market and the research units are the ones that offer analysis of the market. Other investment banks do have an asset management division that does manage money but this is separate to the main advisory and underwriting operations.

The investment banks have different risk exposures since they usually do not use their own capital to make long-range equity investments as PE or VC funds do. Their business model is structured around creating a repetitive flow of deals and nurturing relationships with clients as opposed to having a conglomerate of investments under management over a ten year span. But large investment banks can have principal subsidiaries that conduct proprietary investment in a form that are similar to PE or VC strategies but as part of a corporation. This is why professionals often pursue an Advanced corporate banking and finance course to fully understand the complexities of investment banking compared to PE and VC.

Key Differences in Fund Lifecycle and Capital Deployment

When one looks at the life that investments go through and the strategy of capital deployment, the variations between PE, VC, and IB become most evident. Both VC and Private Equity have limited partnership agreement, with a clear cut capital commitment time, periods of investment and exit schedules. While PE funds inject capital into profitable companies or other assets whose cash flows are predictable, they implement improvements in operations or change in its strategy to add value with the help of the cash injection and sell the target. The investments made by VC funds are of less capital in numerous young companies with hopes that a small percentage of the funded companies would have exponential returns.

Investment Banking, however, does not work towards a fixed lifecycle of investments since it is not a fund in the conventional understanding. Rather, things work out by capital being utilized in a rather roundabout way, and underwriting and facilitating them through market transactions. The IB does not earn revenue due to the maturity of investments but when deals are closed. It makes the IB model more short-term specific rather than long-term oriented management of assets.

The other significant difference is the length of exposure to investments. Patience and a consciously focused guidance are needed to wait and sell the assets in PE and VC funds by the means of the required duration. Investment banks can participate in a transaction only a few months prior to the next transaction and thus there is a higher turnover as well as dependence on new mandates.

Choosing the Right Structure for Different Investment Goals

In the case of investors, knowing the structural variations between PE, VC, and IB is imperative in recognizing the consistency amid capital allocation and the risk resistance, gain anticipation and period of investment. PE may interest those who want consistent, long-term profit exploited by ownership and operational leverage, whereas VC may interest those who can afford to assume increased risk of losing their capital in lieu of massive growth. Individuals or companies interested in increasing capital funds or making business transactions without embarking on attaining long-term ownership interests could use the services of an investment bank.

On one hand, as far as companies in need of the capital are concerned, the partner may influence their path. Fully developed firms which are interested in strategic transformation may seek a PE firm as a source of capital and operating knowledge. Companies that have innovative products may consider their seed investment or growth funding through VC funds. Firms undertaking mergers, acquisitions, or the listings to stock exchange would usually require investment firms to facilitate it with respect to their capabilities of execution and reach to the market.

Finally, it is the financial ecosystem that works best when the three structures pertain to each other and have different functions to be completed in the processes of capital formation, market efficiency, and economic growth. Based on the insights that have been provided on the mechanics and differences of the PE, VC, and IB structure, stakeholders will be better positioned to make decisions concerning where and how to approach the capital markets.